How Does a Life Insurance Payout Work?

Life insurance gives you peace of mind that your loved ones will be financially protected if something happens to you. But many people don’t understand how life insurance payouts actually work — when the money is paid, who receives it, how long it takes, and what options are available.

This guide walks you through the entire process of how life insurance pays out, answers common questions, and explains how to make sure your beneficiaries can receive their payout without delay.

What Is the Life Insurance Payout Process?

The life insurance payout process starts when the policyholder passes away. At this point, the beneficiaries named on the policy need to file a claim with the insurance company. This isn’t automatic — insurance companies typically don’t know someone has died unless notified.

Here’s what the process generally looks like:

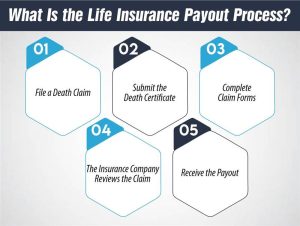

Step 1: File a Death Claim

The beneficiary should contact the life insurance company and notify them of the policyholder’s death. This often involves calling customer service or submitting an online form.

Step 2: Submit the Death Certificate

A certified copy of the death certificate is required to confirm the policyholder’s passing. Without this, the insurer cannot legally process the payout.

Step 3: Complete Claim Forms

The insurer will send a claim packet or provide one online. It includes basic forms asking for personal information and payout preferences.

Step 4: The Insurance Company Reviews the Claim

The insurer checks if the policy is valid, confirms details, and ensures there’s no reason to deny the claim.

How Much Does Life Isurance Cost?

Step 5: Receive the Payout

Once the claim is approved, the insurer issues the death benefit according to the beneficiary’s chosen payout method.

This process usually takes a few weeks but can vary depending on the situation.

How Is Life Insurance Paid Out to Beneficiaries?

When a life insurance policy pays out, the beneficiary gets the death benefit. But how that money is paid can differ based on what the beneficiary chooses. Here are the common payout options:

1. Lump-Sum Payment

This is the most popular method. The full death benefit is paid all at once. It’s straightforward and helps beneficiaries cover funeral costs, debts, and daily expenses right away.

2. Installment Payments

Instead of receiving everything at once, the beneficiary can opt to receive payments over time — for example, over 10, 20, or even 30 years. This method helps manage money more gradually and may earn interest along the way.

3. Annuity

The insurer invests the death benefit and pays a guaranteed income stream for life or for a set number of years. This option is ideal for beneficiaries who want long-term financial stability.

4. Retained Asset Account

Some insurers offer a retained asset account, which functions like an interest-bearing checking account. The beneficiary can withdraw funds as needed using checks, while the rest earns interest.

Choosing the right payout option depends on the beneficiary’s financial situation, comfort with money management, and long-term goals.

How Term Life Insurance Pays Out

Term life insurance provides coverage for a set number of years — such as 10, 20, or 30 years. If the policyholder dies within this period, the insurance company pays the full death benefit to the beneficiary.

- If the policyholder outlives the term, no payout is made, and the policy expires unless it’s renewed.

- The claim process is typically simple and fast, especially for long-standing policies.

- Term policies do not build cash value, so only the death benefit is paid out.

Because of its affordability and simplicity, term life is popular with families looking to protect their income during their working years.

How Whole Life Insurance Pays Out

Whole life insurance is a type of permanent life insurance, meaning it covers you for your entire life as long as premiums are paid. When the insured passes away, the beneficiary receives the death benefit.

- These policies accumulate cash value over time.

- If the policyholder took out loans from the cash value and didn’t repay them, the payout may be reduced.

- Whole life policies often have guaranteed death benefits and fixed premiums.

Some people use whole life insurance for wealth transfer, funeral planning, or estate planning.

Life Insurance Payout Options (Summary Table)

| Payout Option | Description |

| Lump-Sum | Full benefit paid in one tax-free payment. |

| Installments | Equal payments over a fixed period (e.g., 10 or 20 years). |

| Annuity | Pays income for life or a specific number of years. |

| Retained Asset Account | Funds held in an account that earns interest; accessed by checks or withdrawals. |

How Much Does Life Insurance Payout?

Life insurance payout amounts vary depending on the coverage selected by the policyholder. Some policies provide as little as $10,000, while others go up to several million dollars.

Here are some common ranges:

- Term Life Insurance: $100,000 – $1,000,000+

- Whole Life Insurance: $25,000 – $500,000+

- Final Expense Insurance: $5,000 – $30,000 (for funeral/burial costs)

The payout amount is known as the face value or death benefit. It’s typically tax-free for the beneficiary and doesn’t go through probate (unless the estate is the named beneficiary).

What Is the Average Life Insurance Payout?

On average, life insurance payouts in the U.S. fall between $168,000 and $190,000, based on industry data. However, this number depends on the policy type, the insured’s age and health, and how much coverage was purchased.

Final expense policies might pay around $10,000–$20,000, while high-income earners may leave behind $1 million or more in term or permanent coverage.

These funds are often used to:

- Pay off debts or a mortgage

- Cover funeral and burial expenses

- Replace lost income

- Support children’s education

- Leave a legacy or charitable gift

How Long Does It Take for a Beneficiary to Receive Money from Life Insurance?

Most life insurance payouts are made within 2 to 6 weeks after filing the claim, though it can be sooner.

Factors that affect the timeline include:

- Whether all required documents were submitted

- How long the policy has been active

- The cause of death (natural vs. suspicious)

- The insurer’s internal processing speed

Faster Payouts

- Claims on long-standing policies with no red flags

- Electronic submission of documents

- Lump-sum payouts (quicker than annuities or installment options)

Slower Payouts

- Claims during the contestability period (first 2 years)

- If the death involved an accident, suicide, or criminal investigation

- Delays in submitting required paperwork

To avoid delays, it’s best to file a claim promptly and provide a valid, official death certificate.

What Disqualifies a Life Insurance Payout?

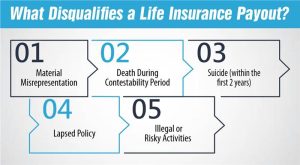

While most claims are paid, some circumstances can lead to denial. Here are the most common disqualifiers:

1. Material Misrepresentation

If the policyholder lied or left out important health or lifestyle details on the application, the insurer may deny the claim.

Example: Claiming to be a non-smoker while smoking regularly.

2. Death During Contestability Period

Most policies have a 2-year contestability period. If the insured dies during this time, the insurer can investigate and potentially deny the claim if misrepresentation is found.

3. Suicide (within the first 2 years)

Many policies have a suicide clause stating that if the insured dies by suicide within the first 1–2 years, no payout is made.

4. Lapsed Policy

If the policyholder stopped paying premiums and the policy lapsed, no death benefit is paid.

5. Illegal or Risky Activities

Death caused by illegal acts, drug overdose, or risky hobbies like base jumping or racing may be excluded, depending on the policy’s terms.

What Is the Time Limit to Claim a Life Insurance Payout?

There’s typically no strict time limit to file a life insurance claim. However, it’s strongly recommended to do so as soon as possible after the policyholder’s death.

Why?

- Some states have statutes of limitation.

- Over time, it may be harder to find the necessary documents.

- Insurers may turn unclaimed death benefits over to the state.

In some cases, beneficiaries may not even know they were listed — which is why it’s so important to communicate your policy details with loved ones.

Tips to Ensure a Smooth Life Insurance Payout

Here’s how to make sure your beneficiaries don’t run into roadblocks when the time comes:

- Keep the policy active – Always pay premiums on time.

- Be honest – Provide accurate info during the application process.

- Update beneficiaries – Review them regularly and after major life changes.

- Store documents securely – Let someone trusted know where to find them.

- Choose a clear payout method – Help your beneficiaries understand their options.

Final Thoughts

A life insurance payout can be a lifeline during one of life’s most difficult moments. Whether you’re a policyholder planning ahead or a beneficiary navigating the process, understanding how payouts work can help you make informed decisions.

- Term life pays out if the insured dies within the term.

- Whole life guarantees a benefit and builds cash value.

- Beneficiaries can choose between lump sum, installments, annuities, or accounts.

- Most payouts are tax-free and arrive within a few weeks.

- Honesty and up-to-date policy info help ensure a smooth process.

If you’re considering life insurance or need help understanding your policy’s payout process, talk to a licensed advisor who can guide you every step of the way.

Need help choosing the right policy or understanding how it works? Contact our team today — we’re here to make life insurance simple and stress-free.

Expert Life Insurance Agent and health insurance agent

Dylan is your go-to guy for life and health insurance at InsureGuardian. He’s helped over 2,500 clients just like you figure out the best insurance plans for their needs. Before joining us, Dylan was sharing his expertise on TV with Global News and making a difference with various charities focused on health. He’s not just about selling insurance; he’s passionate about making sure you’re covered for whatever life throws your way.