Short-Term vs. Long-Term Care Insurance: Costs, Coverage & How to Decide

Introduction

People need to plan for their healthcare requirements, and health insurance acts as an essential tool for maintaining financial stability. Your overall well-being improves when you secure appropriate insurance coverage regardless of unexpected illness or aging conditions. This guideline provides a comparison of short-term against long-term care insurance options to teach you about the distinctions between temporary and sustained healthcare coverage.

The article performs a comparison between short-term care insurance and long-term care insurance, which are separate health insurance products addressing separate duration needs and financial situations. The type of insurance you select depends on your health status combined with your family’s medical background, expense range, and care duration requirements. To make the right choice, you should carefully analyze both short-term health insurance and long-term care coverage because this knowledge will help you select coverage that provides needed assistance without creating enormous financial burdens.

What is Short-Term Care Insurance?

The primary purpose of short-term care insurance lies in delivering temporary health coverage during transient medical requirements. This policy offers temporary coverage, which ranges from several months to one year, and delivers benefits during brief healing and illness durations such as post-surgical recovery.

Key Features of Short-Term Care Insurance

- Coverage for Temporary Medical Needs: Ideal for recovery or rehabilitation, addressing acute health issues.

- Duration: Offers coverage for a few months to one year, making it a flexible option.

- Lower Premiums: More cost-effective compared to long-term care insurance, suitable for short-term needs.

Types of Services Covered

- Rehabilitation: Support for physical therapy and recovery after an injury.

- Post-Surgery Recovery: Financial assistance during healing periods following surgical procedures.

- Short-Term Illnesses: Coverage for temporary conditions that require professional care.

Short-term health insurance benefits people needing temporary healthcare support since it provides needed services at more reasonable prices compared to long-term health policies.

What is Long-Term Care Insurance?

Long-term care insurance makes provisions to support extensive medical care requirements by offering broad coverage for people who have disabilities or chronic illnesses or are aging. The plan delivers monetary help to enable support services that assist with everyday needs together with long-term healthcare management.

Key Features of Long-Term Care Insurance

- Extended Care Coverage: This system extends care over multiple years because of its long-duration design.

- Comprehensive Support: The plan provides extensive health care services that ensure solid long-term care protection.

- Higher Premiums: The wide range of benefits results in higher premiums than those associated with short-term plans.

Types of Services Covered

- In-Home Care: Support for the essential daily tasks that include bathing, dressing the patient, and preparing their meals.

- Assisted Living Facilities: Environments that support individuals who need help with personal care without requiring full-time medical supervision exist separately.

- Nursing Home Care: intensive support in specialized facilities for individuals with severe health conditions.

Choosing between short-term and long-term health insurance coverage, one should select long-term care insurance if they will need constant care all the years of their life.

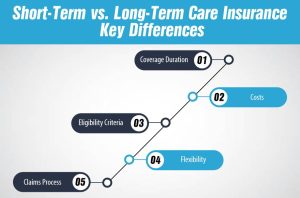

Short-Term vs. Long-Term Care Insurance: Key Differences

The most important thing to know before selecting between short-term care insurance and long-term care insurance is what each of the two has to offer to arrive at the best choice.

How Much Does Life Isurance Cost?

Coverage Duration

- Short-Term Care: Provides coverage for a few months to one year.

- Long-Term Care: Offers coverage for extended periods, often spanning several years.

Costs

- Short-Term Care: People with this insurance type enjoy low premiums but face increased financial responsibility in case their treatment extends beyond usual costs.

- Long-Term Care: This premium-based plan demands higher monthly costs, which results in decreased expenses when looking at the entire plan duration.

Eligibility Criteria

- Short-Term Care: Generally easier to qualify for with fewer restrictions.

- Long-Term Care: This may require detailed medical underwriting with stricter eligibility requirements.

Flexibility

- Short-Term Care: Highly adaptable for temporary health situations.

- Long-Term Care: Structured to provide consistent, long-term support and is less flexible for short-term changes.

Claims Process

- Short-Term Care: Generally features a simplified claims process with faster reimbursements.

- Long-Term Care: involves a more complex process with potentially longer waiting periods.

Cost Analysis: Short-Term vs Long-Term Care Insurance

You must understand the pricing structure thoroughly to compare between short-term and long-term care

Premium Costs

- Short-Term Care: The cost of short-term health insurance premiums ranges between $20 and $100 monthly, making this program attractive for those seeking temporary coverage.

- Long-Term Care: Because the policy includes full coverage benefits, the monthly premiums range from $150 to $300.

Out-of-Pocket Expenses

- Short-Term Care: Higher out-of-pocket costs on deductibles and co-payments tend to be incurred for unexpected conditions that arise.

- Long-Term Care: This coverage becomes more affordable with each passing year, allowing patients to better predict their healthcare expenses during extended treatment.

Influencing Factors

- Age: Older individuals generally face higher premiums.

- Health Condition: Pre-existing conditions can affect both cost and eligibility.

- Policy Features: Additional features such as riders, benefit limits, and inflation protection can also influence premium rates.

Real-Life Cost Example

- Example 1: A person age 45 who selects short-term care insurance policies must spend about $30 in monthly premiums for recovery coverage after surgery.

- Example 2: Starting at the age of 60, an individual is to spend $250 a month to stay covered by a long-term care insurance policy that offers care services at home, as well as assistance for living for several years.

Pros and Cons of Short-Term and Long-Term Care Insurance

Short-Term Care Insurance

Pros:

- Affordable Premiums: Lower costs make it accessible for temporary coverage.

- Flexible Coverage: Ideal for short-term recovery or rehabilitation.

- Quick Approval: Generally faster qualification compared to long-term options.

Cons:

- Limited Duration: Only covers a short period (a few months to one year).

- Not Suitable for Chronic Conditions: May not provide enough support for ongoing, long-term health issues.

Long-Term Care Insurance

Pros:

- Comprehensive Coverage: offers extensive long-term care coverage for chronic and aging-related needs.

- Peace of Mind: Reduces financial stress by covering prolonged care requirements.

- Broad Service Range: Covers in-home care, assisted living, and nursing home care.

Cons:

- Higher Premiums: More expensive due to the breadth of coverage.

- Complex Eligibility: Stricter criteria based on age and health conditions can limit accessibility.

It is always important to analyze the advantages and disadvantages of short-term health insurance to identify the plan that will meet your healthcare needs and financial goals most appropriately.

How to Decide Between Short-Term and Long-Term Care Insurance

Some of the factors one has to take into consideration regarding their lifestyle apart from finance include the type of insurance policies to opt for, whether short-term or long-term care insurance plans.

- Assess Personal Health and Family Medical History: Assess your current health status and genetic conditions or tendencies when experiencing chronic health conditions. An even greater actual sensitivity to long-term health complications means that the use of long-term care insurance may be beneficial.

- Review Your Financial Situation: The evaluation of your financial budget should include your future long-term financial targets. The purchase of short-term care insurance at a lower premium amount will not pay for complete long-term care costs.

- Determine Your Risk Tolerance: To decide what healthcare approach suits you best you need to determine your feelings regarding future health dangers. People seeking extensive healthcare protection instead of worry-free medical care should opt for extended-term plan options.

- Consult with Insurance Advisors: Get in touch with professionals who will prepare specific advice suited to your particular condition. Health insurance specialists will direct you toward selecting the most appropriate coverage from either short-term plans or standard policies.

FAQs

What is the difference between short-term and long-term health insurance?

Coverage for 12 months targets people with particular needs for short-term health insurance. Long-term care insurance, by contrast, keeps the policyholder safe from chronic health issues requiring ongoing nursing care and services.

Which is better: short-term or long-term care insurance?

It depends on your problem. People who require help during short-term healthcare emergencies will benefit from short-term care insurance, while those with long-term ailments will best enjoy long-term care insurance.

Can I have both short-term and long-term care insurance?

Some individuals prefer the coverage that comes from both short-term and long-term care insurance. While short-term care insurance deals with immediate needs, long-term care insurance creates a protective network to deal with prolonged future needs.

Conclusion

The major decision between short-term and long-term care insurance depends entirely on how well you understand your health situation along with your financial situation and long-lasting healthcare requirements. Temporarily protected healthcare needs to find proper coverage through short-term care insurance, but long-term care insurance provides extensive coverage duration for chronic disease management.

Create your choice from two options through an evaluation of your medical history and your willingness to take risks against your current financial resources. Obtaining professional insurance advice leads to optimal outcomes because these experts can analyze your requirements to match you with the right healthcare plan.

Expert Life Insurance Agent and health insurance agent

Dylan is your go-to guy for life and health insurance at InsureGuardian. He’s helped over 2,500 clients just like you figure out the best insurance plans for their needs. Before joining us, Dylan was sharing his expertise on TV with Global News and making a difference with various charities focused on health. He’s not just about selling insurance; he’s passionate about making sure you’re covered for whatever life throws your way.