Variable Whole Life Insurance Can Be Described As a Flexible Investment and Protection Plan

Introduction

Research shows that 67% of policyholders have a poor understanding regarding their life insurance cash value accumulation. The combination of protection and investment advantages makes it difficult for people to understand such policies, especially those that encompass both features. Variable whole life insurance serves as a financial product that provides continuous protection together with an opportunity to increase wealth accumulation.

Most individuals find it difficult to understand the operational mechanism of hybrid insurance products. People frequently inquire about policies that guard their families and build wealth simultaneously. The fundamental structure behind variable whole life insurance (VWLI) provides the solution.

What Is Variable Whole Life Insurance?

Variable whole life insurance exists as permanent insurance that combines death benefit protection with market-based investment features. The insurance policy provides life-long death benefit protection while its built-up cash value grows according to underlying investment performance.

The primary objectives of variable whole life insurance include offering death benefits to beneficiaries and enabling policyholders to accumulate wealth while making investments. VWLI remains active for your lifetime since you must continuously pay premiums, while term life insurance offers coverage for only a designated period. VWLI offers a perfect choice for people who need extended financial planning due to its indefinite duration.

Key Comparisons:

- VS. Traditional Whole Life: Fixed returns vs. market-linked growth. Whole life insurance provides members with certain fixed investments in their cash value accumulation. The performance of your investment sub-accounts at VWLI determines your earning potential because it differs from the fixed returns of whole life insurance policies.

- VS. Variable Universal Life (VUL): Guaranteed premiums vs. flexible payments. Fixed premiums in Variable whole life insurance plans create steady financial costs in your budget, while Variable universal life insurance policies allow policyholders to determine payment amounts unpredictably.

Key Features of Variable Whole Life Insurance:

- Market-Linked Cash Value: Stock and bond investments and mutual fund purchases direct policy funds for market-based growth in your cash value. The growth potential from this feature allows policy value expansion, but market volatility will affect your cash value amounts.

- Fixed Premiums: The fixed premium structure of variable whole life insurance gives your financial planning a predictable structure through which you can manage payments. After paying your monthly premium amount, you will get complete clarity on your budget management due to your knowledge of the required payment.

- Lifetime Coverage: Your loved ones will always receive the death benefit payment because your coverage stays consistent with market movements. Your beneficiaries will receive a death benefit payout from your life insurance regardless of changes in the market after you die.

- Regulated as a Securities Product: Variable whole life insurance exists under dual regulation because it combines substantial insurance protection with securities features, which brings extra protections to policyholders. The regulatory system maintains transparency as well as accountability in the management processes for your policy.

How Variable Whole Life Insurance Works (Step-by-Step):

- Choose Your Policy and Premium Amount: Choose a coverage plan that is convenient in terms of the details you need and your budget. It means that one needs to consider some things, such as income, his/her family’s requirements, and the financial status that he/she has for the future.

- Allocate Premiums to Investment Sub-Accounts: Within your premium payments, some funds are invested through stocks, bonds, and mutual funds. The policyholder can select from different sub-account options that match their risk tolerance level and financial plans.

- Cash Value Grows Based on Market Performance: The amounts you invest will directly affect how your account value increases during the time. Market performance directly affects cash value growth since strong or weak market performance results in either substantial growth or value reduction.

- Tax-Free Loans/Withdrawals from Cash Value: Tax-free benefit withdrawals or loans help you access the cash value within your policy whenever you need funds. The policy’s cash value serves as an amazing financial tool because it enables you to borrow funds for emergencies or to fund educational needs or other financial requirements.

Flowchart:

Premium → Investment → Cash Value → Death Benefit

VWLI ensures your loved ones gain permanent life insurance protection from the moment you purchase it until your lifetime concludes. The product combines permanent life insurance with financial investment capabilities. Each premium payment allocates funds to investment accounts comprising stocks and bonds, which let your cash value increase as time passes. The cash value increases through investments whose performance determines the potential growth and security of the account.

Your family needs security from VWLI without forfeiting the chance to build financial wealth. VWLI provides a method to combine investment growth with lifelong protection benefits in a single solution. Studying VWLI will enable you to make wiser money decisions that give you both safety and peace of mind.

How Much Does Life Isurance Cost?

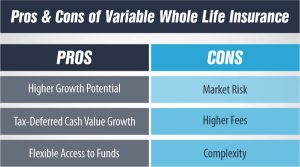

Pros and Cons of Variable Whole Life Insurance:

Pros:

- Higher Growth Potential: Another benefit of variable life insurance is relatively better growth performance compared to traditional whole life insurance because of market-linked investment.

- Tax-Deferred Cash Value Growth: Your money can earn interest without being taxed until you cash in, and that’s considered giving back, hence the name retirement savings.

- Lifelong Coverage: The policy gives you security by assuring your beneficiaries will get their death benefit independent of your death date.

- Flexible Access to Funds: Insurance policyholders have the opportunity to borrow tax-free funds from their cash reserves for personal expenses.

Cons:

- Market Risk: Your cash value depends on market performance and may decrease due to market fluctuations. No returns are guaranteed.

- Higher Fees: VWLI insurance features increased expenses related to both management and administration compared to standard term life insurance.

- Complexity: Handle your policy and find suitable investment choices through valid financial guidance because these tasks tend to be complex.

Who Should Buy Variable Whole Life Insurance?

VWLI is ideal for:

- Long-Term Planners: Individuals who concentrate on achieving legacy goals with financial considerations.

- High-Risk Tolerance Investors: People who have an appetite for market changes seek higher growth potential.

- Estate planning needs: those who want to build financial legacies while potentially growing their assets.

Not ideal for:

- Short-Term Coverage Seekers: Term life insurance provides better value to people requiring short-term protection.

FAQs

Which statement is true regarding a variable whole-life policy?

A variable whole life insurance policy provides complete longevity coverage and lets policyholders manage their investments through their accounts. A variable whole life insurance policy lets you access market-linked sub-accounts through its death benefit guarantee. Your policy cash value grows through the market performance of the investments your policy is tied to. Therefore, you obtain security benefits and investment capability.

What is the best description of variable life insurance?

The hybrid insurance product Variable Life stands as a permanent insurance policy with cash value components that rely on market performance. The contribution system of variable life insurance differs from fixed policies because VWLI allows you to invest premium funds into diverse investment options. Your cash value-building potential increases over time because of this opportunity, which provides both lifelong protection and additional financial potential.

Can I lose money in a variable whole-life policy?

A variable whole-life policy contains an investment portion, which means your money may decrease in value because the cash value depends on market fluctuations. The unlike death benefit is secure, but the investment value of the policy experiences market ups and downs. Understanding your risk tolerance becomes essential because variable whole-life policies create both opportunities to build value and possibilities of value reduction.

Conclusion

It may be defined as permanent life insurance that offers coverage for the whole lifetime and also acts as an investment tool for people’s prosperity. It is a versatile life insurance product that has the feature of a permanent life insurance plan with an investment element linked to a specific market or stock exchange. Option for life, fixed premiums, lifelong coverage, and even a component of investment make VWLI the perfect way to plan for the future.

Expert Life Insurance Agent and health insurance agent

Dylan is your go-to guy for life and health insurance at InsureGuardian. He’s helped over 2,500 clients just like you figure out the best insurance plans for their needs. Before joining us, Dylan was sharing his expertise on TV with Global News and making a difference with various charities focused on health. He’s not just about selling insurance; he’s passionate about making sure you’re covered for whatever life throws your way.