Can You Switch from Term to Whole Life Insurance?

Introduction

Life insurance is an essential part of financial planning, but your needs may change over time. Many people start with term life insurance because it’s affordable, but later, they may want permanent coverage. This raises the question: Can you switch from term to whole life insurance? The answer is yes—many term life insurance policies include a conversion option that allows you to transition to a whole life policy without a medical exam. In this article, we’ll explore how this works, why you might consider it, the costs involved, and the alternatives available.

How Does Convertible Term Life Insurance Work?

Convertible term life insurance is a policy that allows you to switch from term to whole life insurance before the term ends. Here’s how it works:

- Built-in conversion option: Many term life policies include a conversion feature that lets you upgrade to whole life insurance without proving insurability.

- No medical exam required: Unlike applying for a new policy, converting doesn’t require you to undergo a medical check-up, which is beneficial if your health has declined.

- Time limitations: Most insurers allow conversions only within a specific period, such as the first 10 or 15 years of the term policy. If you miss this window, you might have to undergo underwriting to qualify for a new whole life policy.

- Higher premiums: Since whole life insurance is more expensive than term insurance, your monthly or annual payments will increase after conversion.

- Partial conversions: Some insurers allow you to convert only a portion of your term policy, enabling you to keep some affordable term coverage while gaining the benefits of whole life insurance.

Understanding these details can help you determine if conversion is the right move for your financial future.

Why Would You Consider Converting Term Life to Whole Life Insurance?

There are several reasons why switching from term to whole life insurance might be beneficial:

- Lifelong Coverage: Whole life insurance offers lifetime protection, ensuring your family receives a death benefit regardless of when you pass away. This is ideal if you want to secure your loved ones’ financial future for the long term.

- Cash Value Growth: Whole life policies accumulate cash value over time, which you can borrow against or withdraw for emergencies. This makes it a financial asset that grows tax-deferred.

- Estate Planning: If you want to leave an inheritance or cover estate taxes, whole life insurance can be a strategic financial tool. It can also be used to fund trusts for beneficiaries.

- Changing Responsibilities: Life events such as having children, buying a home, or starting a business may create a need for lifelong financial security. As your responsibilities grow, having permanent life insurance can offer peace of mind.

- Retirement Supplement: The cash value in a whole life policy can be used as a supplemental retirement income source through policy loans or withdrawals.

If your financial goals have shifted since purchasing your term policy, converting to whole life insurance might be a wise decision.

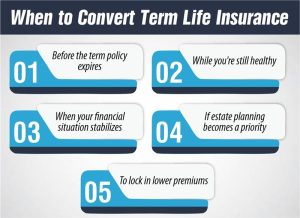

When to Convert Term Life Insurance

Timing is crucial when deciding to convert from term to whole life insurance. Here’s when you should consider making the switch:

- Before the term policy expires: Once your term policy ends, you may lose the conversion option, leaving you without coverage or requiring a new application with a medical exam.

- While you’re still healthy: Although conversions don’t require a medical exam, some policies have age restrictions. Waiting too long could mean higher premiums or limited conversion options.

- When your financial situation stabilizes: Since whole life insurance is more expensive, ensure you can handle the higher premiums before converting.

- If estate planning becomes a priority: If you accumulate wealth or have dependents, converting can help secure your financial legacy. Whole life insurance is often used to cover estate taxes and ensure a smooth transfer of assets.

- To lock in lower premiums: Converting sooner rather than later allows you to secure a lower rate, as premiums are based on your age at the time of conversion.

If you wait too long, you might lose the chance to convert, forcing you to buy a new policy that could be more expensive.

How Much Does It Cost to Convert from Term Life to Whole Life?

The cost of converting a term life policy to whole life insurance depends on several factors:

How Much Does Life Isurance Cost?

- Premium Differences: Whole life insurance costs significantly more than term life because it includes a savings component. Expect a premium increase after conversion.

- Age at Conversion: The older you are, the higher your premiums will be. Converting early can help reduce costs.

- Policy Features: Some whole life policies have additional benefits, like dividend payouts or riders, which can influence costs.

- Partial vs. Full Conversion: Some insurers allow partial conversions, meaning you can convert a portion of your term policy and keep some term coverage to manage costs.

- Additional Fees: Some insurance companies may charge a conversion fee, although many waive it if the conversion occurs within the designated period.

It’s best to compare quotes from your insurer before deciding to ensure affordability.

Pros and Cons of Convertible Term Life Insurance

Pros

- No medical exam required – Beneficial if your health has worsened since you bought your term policy.

- Lifelong coverage – Ensures financial protection for your beneficiaries.

- Cash value accumulation – Provides a savings component that can be used later in life.

- Estate planning benefits – Helps cover estate taxes and leave an inheritance.

- Locked-in premium rates – Your whole life premiums remain fixed, providing cost certainty.

Cons

- Higher premiums – Whole life insurance costs significantly more than term life.

- Limited conversion period – You must convert within a certain timeframe.

- May not be necessary for everyone – Some people may find better investment options elsewhere.

- Less flexibility – Whole life policies can be rigid compared to other investment vehicles.

If you’re unsure whether to convert, weigh the pros and cons carefully based on your financial needs.

Alternatives to Switching from Term to Whole Life Insurance

Converting your term policy isn’t the only option. Here are a few alternatives:

- Buy a New Whole Life Policy: Instead of converting, you can apply for a new whole life policy. However, this may require a medical exam and higher premiums.

- Renew Your Term Policy: Some term policies offer a renewal option that extends coverage without switching to whole life. However, renewal premiums increase with age.

- Invest the Difference: Instead of paying higher whole life premiums, you can invest the extra money in stocks, bonds, or retirement accounts for potentially greater returns.

- Consider a Universal Life Policy: If you need flexibility, a universal life policy might be a better fit than traditional whole life insurance. Universal policies allow you to adjust premiums and death benefits over time.

- Layering Policies: Some people keep their term policy and purchase a small whole life policy to cover final expenses while investing the rest elsewhere.

These alternatives might provide similar benefits without the high costs of conversion.

Frequently Asked Questions (FAQs)

1. Can I convert my term life insurance to whole life insurance at any time?

No, most term policies have a specific conversion period, typically within the first 10–15 years of the policy. Check with your insurer for the exact timeframe.

2. Do I need a medical exam to convert my policy?

No, one of the main benefits of converting is that it does not require a medical exam, even if your health has worsened.

3. Will my premiums increase after converting to whole life insurance?

Yes, whole life insurance premiums are significantly higher than term life premiums because of the lifelong coverage and cash value component.

4. Can I convert only part of my term life insurance policy?

Yes, many insurers allow partial conversions, meaning you can convert a portion of your term policy while keeping the rest as term coverage.

5. What happens if I don’t convert my term life insurance before it expires?

If your term policy expires and you haven’t converted, you may need to buy a new policy, which could require a medical exam and higher premiums.

6. Are there alternatives to converting term life to whole life insurance?

Yes, alternatives include buying a new whole life policy, renewing your term policy, investing the difference, or considering a universal life policy.

7. Is converting to whole life insurance worth it?

It depends on your financial goals. If you need lifelong coverage, cash value accumulation, and estate planning benefits, it can be a good choice. However, if affordability is a concern, investing the difference might be a better option.

Conclusion

Switching from term to whole life insurance can be a smart move if your financial priorities have changed. The conversion option allows you to gain lifelong coverage and cash value benefits without a medical exam. However, it comes with higher premiums and must be done within a specific timeframe.

Before making the switch, evaluate your financial goals, compare costs, and explore alternatives. Consulting with an insurance professional can help you make the best decision for your future.

Do you need help choosing the right life insurance policy? Speak with an expert today!

Expert Life Insurance Agent and health insurance agent

Dylan is your go-to guy for life and health insurance at InsureGuardian. He’s helped over 2,500 clients just like you figure out the best insurance plans for their needs. Before joining us, Dylan was sharing his expertise on TV with Global News and making a difference with various charities focused on health. He’s not just about selling insurance; he’s passionate about making sure you’re covered for whatever life throws your way.