How Does Life Insurance Provide Tax Advantages? Complete Guide

Would you like to keep your loved ones secure if anything happens to you and also want to save some money off your taxes? Life Insurance can be the best solution for you. Aside from providing your family with economic security, various life insurance tax advantages will improve your PER.

In this guide, we will find out how life insurance will help you save on taxes while providing both immediate and long-term benefits.

What are the Life Insurance Tax Advantages?

Like any other insurance policy, life insurance tax advantages might be useful in your plans. One of the most important benefits which come with the policy is that the death benefit is paid directly to your beneficiaries tax-free by the federal income tax. It means your loved ones get the whole amount without being minimally deducted to help them in terms of financial aspects.

Permanent life insurance plans including whole and universal life accumulate cash value over the long term. This cash value does not accrue taxes and expands more rapidly while in your policy. You can use this cash value when you are alive as well as borrow against it during your policy term.

However, there could be some estate taxes regarding life insurance, yet, some of them can be avoided, in case you apply some certain measures, such as the irrevocable life insurance trust (ILIT). An ILIT can be useful in the sense that it helps to reduce the death benefit from the estate for taxation.

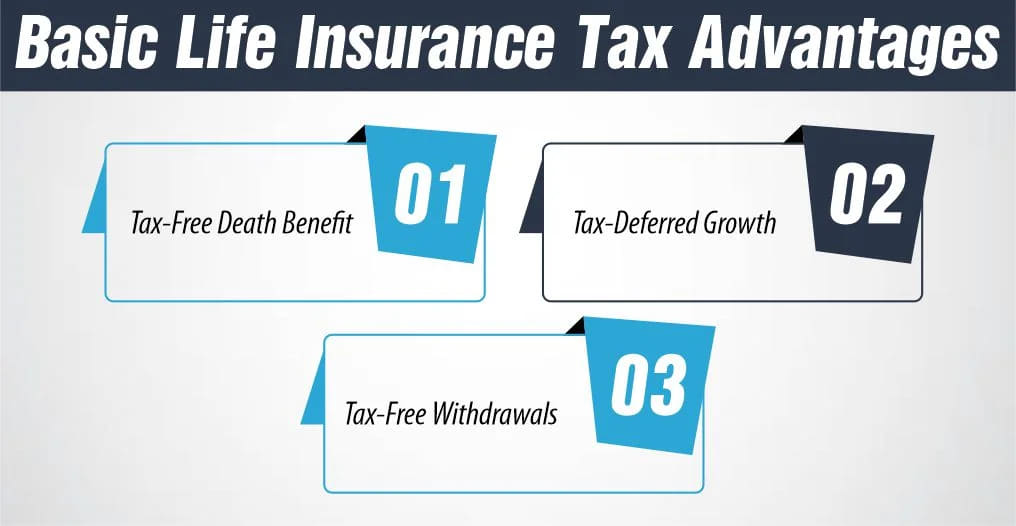

Basic Life Insurance Tax Advantages

Life insurance has 3 basic tax advantages making it a valuable part of your financial planning. These are:

1- Tax-Free Death Benefit

The amount received by the insured’s beneficiaries when he dies, such as the death benefits, is not federally taxable. It helps your loved ones to get the death benefit in full without being charged, which will be good financial support in such an unfortunate period.

2- Tax-Deferred Growth

The cash value feature in permanent life insurance also grows on a tax-deferred basis. It means you cannot be taxed on the yields that this policy earns for you in terms of interest, dividends and gains until you withdraw it. In this way, the taxes are paid later, and the cash value grows in a better way as time passes.

3- Tax-Free Withdrawals

Any withdrawals from the cash value component of a permanent life insurance plan is not taxable up to the amount of the premium paid. It allows you to access the cash without appealing adverse tax implications at the early stages.

Other Life Insurance Tax Advantages

Other Life Insurance Tax Advantages

Other Life Insurance Tax Advantages

Other Life Insurance Tax Advantages Aside from these 3 major life insurance tax advantages, here are some other benefits worth mentioning:

1. Tax-Free Loans

Some but not all types of permanent life insurance policies allow policyholders to borrow against the policies’ cash value without paying taxes. These policy loans are also not regarded as taxable income as long as they do not exceed the total premiums paid. It would allow the possibility of withdrawing funds during times of need but without being taxed for it.

How Much Does Life Isurance Cost?

2- Estate Tax Benefits

Life insurance can also help you in the management of estate taxes. Your policy’s death benefit pays the estate taxes to ensure that your loved ones receive the full estate. Also, strategic planning can exclude the amount received through life insurance compensations from the taxable estate, thus reducing the overall tax burden.

3- Charitable Contributions

When you designate a charity as the beneficiary of your policy’s death benefits, you regard the death benefit as a charitable contribution. This can bring about a good tax credit because it helps to reduce the taxes on the estate and also supports a cause in which you have an interest.

How Maximum Funded Tax-Advantaged Life Insurance?

Max-funded Indexed Universal Life Insurance (IUL) is a permanent life insurance product that invests in an external index strategy to determine the interest rate credited to the cash value. It focuses on the premiums paid, aiming at maximizing cash value accumulation while maintaining a low cost of life insurance.

But the question is how maximum funded tax-advantaged life insurance. Well! Max-funded IUL is a policy where you supplement your premiums to the maximum allowed yearly contribution, which goes beyond covering the cost of your life insurance. Such high premiums provide funds to the policy which in turn gains cash value through interests given based on the S&P 500, for example.

Especially, IUL provides basic guarantees on returns, to maintain the cash value from current market fluctuation while enabling you to share in only the upside. This downside protection makes over-funding an IUL even more attractive to a second group of investors who are willing to sacrifice both the high death benefit and extra premium crediting for lifetime benefits that an indexed universal life insurance policy can bring to them.

Furthermore, the tax benefits received from max-funded IUL policies further increase the efficiency of the policies, thereby providing considerable income tax advantages, making itself ideal for those who seek efficient tax-protected investments.

How Does Whole Life Insurance Provide Tax Benefits?

Whole life insurance provides a convenient option for those who need to set up a savings account that will be free from taxes. However, the money you save inside your cash value account can earn interest and other returns on a tax-favored basis, meaning you don’t have to pay income tax as long as the money remains within the policy.

This is not the same as putting money in a savings account or a Certificate of Deposit at a bank, where the bank usually subjects some amount of that interest to you annually. Also in case you decide to get a loan on cash value in your whole life insurance policy, you can be able to use this money without being taxed on that amount.

How to Calculate the Universal Life Insurance Tax Advantages?

The calculator shows you how much return a universal insurance plan is likely to generate. Meanwhile, your expected return rate depends on your policy amount and your company’s investment, your policy premiums and the taxes that are prevailing at the time of your benefit collection. Your universal life insurance policy has a beneficiary to receive a payment in case you die, and coverage stays for as long as payments are made.

Making calculations, you estimate a premium depending on your age and your health characteristics. For this, you can use our calculator to get an estimate of the tax advantages of a universal life insurance plan. Simply put the required information and you are all set to have a calculation.

The Bottom Line

In the end, life insurance can help you avoid paying taxes in all these ways that have been outlined and also help the beneficiaries with their taxes. It means that upon the policyholder’s death, all beneficiaries receive their entitled share without the tax deduction. Many Americans consider it more efficient than simple savings because it invests the cash value component with deferred taxes.

Also, Tax-Free withdrawals and loans allow for the additional possibility of taking your funds without worrying about taxes. It is worth noting that life insurance tax advantages play a crucial role in everyday life when you get to understand when and how to apply these options in your finance planning to make sure that your family is secure forever. So, more than just protection, the policy is also a way to effectively manage tax.

Expert Life Insurance Agent and health insurance agent

Dylan is your go-to guy for life and health insurance at InsureGuardian. He’s helped over 2,500 clients just like you figure out the best insurance plans for their needs. Before joining us, Dylan was sharing his expertise on TV with Global News and making a difference with various charities focused on health. He’s not just about selling insurance; he’s passionate about making sure you’re covered for whatever life throws your way.