Life Insurance Build Chart: Dynamics, Facts, and Solutions

What is a Life Insurance Build Chart?

A Life Insurance Build Chart, also known as a height and weight chart or build table, is a tool utilized by insurance underwriters to assess an individual’s health and determine their eligibility for life insurance coverage. It establishes a correlation between an individual’s height and their ideal weight range, offering guidelines for insurance companies to evaluate an applicant’s health status.

This chart typically outlines specific weight ranges considered appropriate or healthy for different heights. By comparing an individual’s actual weight to the suggested weight range for their height, insurers use these charts as one of the metrics to gauge potential health risks associated with an applicant. It helps underwriters make informed decisions regarding insurance premiums, coverage, or even the approval of an insurance policy.

Understanding the Life Insurance Build Chart Dynamics

Understanding the dynamics behind a Life Insurance Build Chart is fundamental when navigating the complex world of life insurance. These charts, often deemed as height and weight guidelines, carry more depth than a mere comparison of numbers. They form a pivotal part of the insurance underwriting process, shedding light on an applicant’s health, potential risks, and insurability.

The dynamics of a Life Insurance Build Chart lie in its ability to establish a correlation between height and weight, presenting a range considered ideal or healthy for each height category. But it’s not just about fitting into a specific weight range for your height; it’s about deciphering how these numbers influence insurance decisions.

Insurance companies use these charts to assess an applicant’s health status. Deviations from the suggested weight range for a particular height might signal potential health risks, impacting insurance premiums or even eligibility for coverage. However, these charts aren’t the sole determinants. They are part of a broader evaluation that includes various health factors, aiming to ensure a fair assessment of an individual’s health and risk profile.

Life Insurance Weight Chart Based On Height:

Life insurance weight charts based on height outline the optimal weight range corresponding to different heights. For instance, a person who is 5 feet 8 inches tall might have an ideal weight range of 140-180 pounds according to a typical insurance build chart. Deviations from this range could impact insurance assessments.

Here is an example of a Life Insurance Weight Chart based on height:

How Much Does Life Isurance Cost?

| Height (Feet-Inches) | Ideal Weight Range (Pounds) |

| 5’0″ | 100 – 135 |

| 5’2″ | 110 – 145 |

| 5’4″ | 120 – 155 |

| 5’6″ | 130 – 165 |

| 5’8″ | 140 – 175 |

| 5’10” | 150 – 185 |

| 6’0″ | 160 – 195 |

| 6’2″ | 170 – 205 |

| 6’4″ | 180 – 215 |

Please keep in mind that this table represents a generalized example. Actual Life Insurance Weight Charts can vary significantly between insurance companies and may include additional factors or categories. Individuals seeking insurance should consult with specific insurance providers to understand their particular guidelines and assessment criteria.

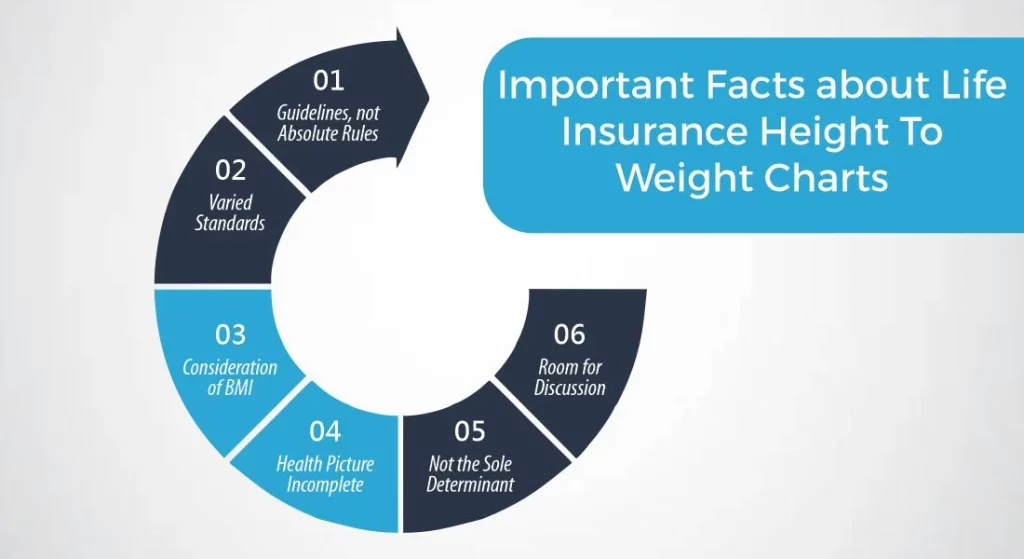

Important Facts about Life Insurance Height To Weight Charts

Here are some important facts about Life Insurance Height to Weight Charts:

1- Guidelines, not Absolute Rules

Height to Weight Charts in life insurance serve as guidelines rather than strict rules. They provide a general overview of ideal weight ranges corresponding to specific heights. Deviations from these ranges don’t automatically disqualify applicants but might warrant further assessment.

2- Varied Standards

Different insurance companies may have their own unique Height to Weight Charts. These variations can affect how insurers assess an individual’s health and eligibility for coverage. It’s crucial to understand the specific guidelines used by the insurer you’re applying to.

3- Consideration of BMI

While Height to Weight Charts focus on these two factors, insurers often consider the Body Mass Index (BMI) as an additional metric. BMI uses height and weight to estimate body fat and can influence the assessment of an applicant’s health risk.

4- Health Picture Incomplete

Height and weight alone don’t paint a comprehensive health picture. Factors such as muscle mass, bone density, and overall health condition should be considered, as they can impact an individual’s health despite variations in weight for a given height.

5- Not the Sole Determinant

Height to Weight Charts are just one aspect of the evaluation process. Insurers assess multiple health-related factors to determine an applicant’s overall risk profile and eligibility for life insurance coverage.

6- Room for Discussion

If an applicant falls outside the suggested weight range for their height, providing additional health-related information or undergoing medical examinations can help in demonstrating good health and eligibility for coverage.

BMI for Life Insurance

Body Mass Index (BMI) is a widely used measure by insurance companies to assess an individual’s health risk when applying for life insurance. BMI is calculated based on a person’s height and weight and provides a numerical value that categorizes individuals into different weight status categories, such as underweight, normal weight, overweight, or obese.

For life insurance purposes, BMI serves as an additional metric alongside Height to Weight Charts to evaluate an applicant’s health and potential risk factors. Insurance companies often use BMI as a quick screening tool to estimate body fat and assess the likelihood of certain health conditions associated with higher body weights.

It’s important to note that while BMI is a convenient tool, it has limitations. It doesn’t differentiate between fat and muscle mass, potentially categorizing muscular individuals as overweight or obese when they’re actually healthy and fit. Therefore, some insurers may consider additional health assessments or medical examinations to gain a more comprehensive understanding of an applicant’s health beyond BMI calculations.

Applicants should be aware of their BMI and understand how it factors into the insurance evaluation process, knowing that while it’s a consideration, it’s not the sole determinant of an individual’s health or insurance eligibility.

Expert Life Insurance Agent and health insurance agent

Dylan is your go-to guy for life and health insurance at InsureGuardian. He’s helped over 2,500 clients just like you figure out the best insurance plans for their needs. Before joining us, Dylan was sharing his expertise on TV with Global News and making a difference with various charities focused on health. He’s not just about selling insurance; he’s passionate about making sure you’re covered for whatever life throws your way.