Are you looking for a way to make your life insurance work harder for you? Under an interest sensitive whole life policy, your money isn’t just sitting around—it’s actively growing. This type of policy adjusts with the market, which means your savings could increase as interest rates rise. Plus, you have the flexibility to adjust your payments according to your financial situation. Isn’t it time your life insurance did more than sit there? Let’s dive into how an interest-sensitive whole life policy can be a smart move for securing your financial future.

Interest sensitive whole life policy

Under an interest sensitive whole life policy is like having a reliable life insurance plan with a bonus feature.

This type of insurance is like your lifelong financial buddy with a neat twist: the money you tuck away can grow, and how much it grows depends on the economy’s performance.

Picture this: you pay a regular monthly amount, just like you would with any standard life insurance. Some of that money ensures you are blanketed, and the relaxation is going right into a financial savings pot. But here’s where it receives thrilling—the quantity on this financial savings pot doesn’t just sit there; it grows. And the rate at which it grows can change with the economic system, every so often going up, once in a while dipping down, kind of like a roller coaster experience!

Plus, there is a sweet extra gain: you can use this cash even as you’re nevertheless around. Need some coins for an unexpected rate or a prime purchase? You can borrow from your policy without any fuss.

So, if you’re into the idea of defensively protecting your family while additionally making your money work harder for you, this policy might be exactly what you want. It’s absolutely the best of both worlds—supplying you with protection and the risk for a few increases.

Understanding Interest Sensitive Life Insurance

Interest sensitive life insurance is a bit like your classic life insurance’s more flexible cousin. It offers the lifelong protection you expect but with a twist—the cash value of your policy can grow based on current interest rates, making it a potentially more lucrative option.

What Sets It Apart from Traditional Policies?

Traditional whole life insurance policies are like the reliable friends of the insurance world—always steady and dependable. You pay a set amount each month, which covers your insurance and also goes into a savings part of the policy. This savings grows at a fixed rate that doesn’t change. Simple and stable.

Enter interest sensitive life insurance. It shakes things up by tying the growth of your cash value to the performance of interest rates in the economy. This means that when interest rates soar, so could the growth of your cash value. More risk? A bit. More potential reward? Absolutely.

Why Consider Interest Sensitive Life Insurance?

Why Consider Interest Sensitive Life Insurance?

Why Consider Interest Sensitive Life Insurance?

Why Consider Interest Sensitive Life Insurance?- Adaptability: As interest rates change, so does the growth rate of your policy’s cash value. This can be great in a booming economy.

- Stable Premiums: Despite the fluctuating nature of your cash value growth, your premiums remain fixed. This makes budgeting straightforward while allowing your savings potential to fluctuate with the economic tides.

- Access to Cash: Need money for a major expense? You can borrow against the cash value of your coverage without jumping through hoops. It’s like having an economic protection net that you may really use when life throws a curveball.

- Long-Term Security: At its core, it’s nevertheless lifestyle coverage. Because of this, it affords a demise benefit to your family regardless of when you pass away.

Interest sensitive life insurance is ideal for individuals who admire a bit of a bet for potentially higher returns but costs the security and permanence of conventional life coverage. It’s like having your cake and ingesting it, too—with the introduced possibility of your cake getting bigger over the years! If you’re comfortable with the United States and the downs of the economy and just like the idea of your coverage working a piece more challenging for you, this can be an appropriate blend of threat and reward.

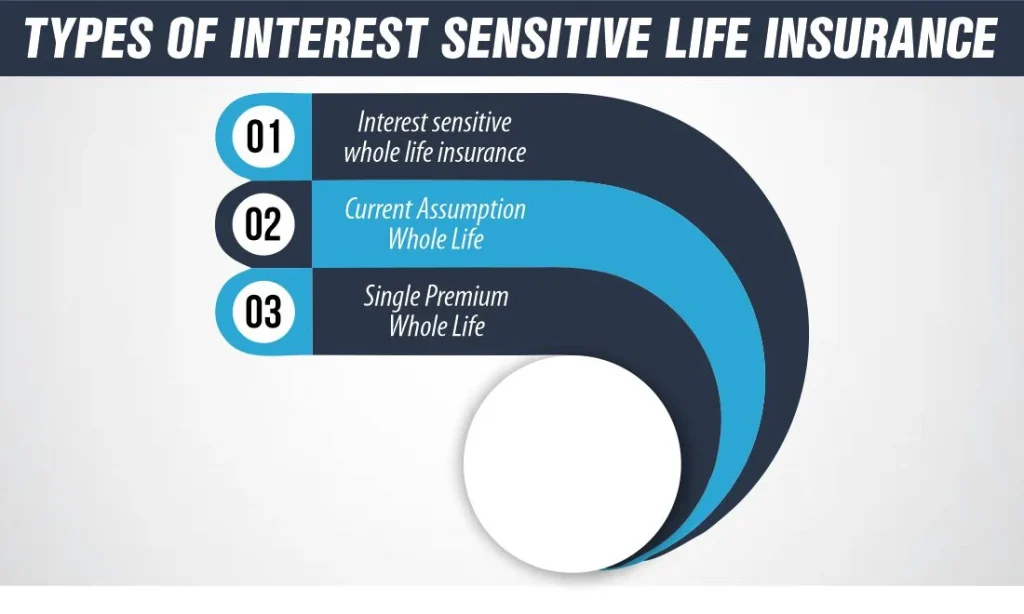

Types of Interest Sensitive Life Insurance:

Types of Interest Sensitive Life Insurance:

Types of Interest Sensitive Life Insurance:

Types of Interest Sensitive Life Insurance: Interest sensitive whole life insurance

Interest sensitive whole life insurance adjusts with the economy, so your savings can grow when interest rates go up. You can also change how much you pay based on your current financial situation, making it easier to manage. Within this category, there are a couple of popular policies:

Current Assumption Whole Life:

Current Assumption Whole Life (CAWL) is like the adaptable, easy-going friend who continuously checks the weather and adjusts plans accordingly. The main draw here is the flexibility in the interest rate applied to the policy’s cash value, which adjusts based on the economic climate. This means that when interest rates are high, you could see a significant boost in your policy’s cash value.

Key Features:

Flexible Premiums: Initially, you might pay a standard premium, but over time, these can adjust. The goal is to maintain enough to cover the costs of insurance while allowing the rest to grow.

Adjustable Death Benefit: Depending on the policy’s performance and your preferences, you can tweak the death benefit. This is particularly handy if your financial situation or insurance needs change over time.

Interest Rate Adjustments: The interest rate on the cash value can increase or decrease based on economic conditions, making it responsive to inflation and other financial trends.

Single Premium Whole Life:

Think of Single Premium Whole Life (SPWL) as the “one and done” approach to life insurance. You make a single, substantial payment upfront, and in return, you get a life insurance policy fully paid up for life. It’s like buying your peace of mind in one go.

Key Features:

Immediate Cash Value: Since you pay the entire premium at once, the policy has significant cash value right from the start. This cash can grow over time, depending on the interest rates, giving you a nice financial cushion.

Fixed Death Benefit: The death benefit is typically set at the time of purchase and doesn’t require further premiums. It’s a straightforward, no-fuss approach to securing a legacy.

Loan Options: The policy has a robust cash value from day one, so you can borrow against it if you ever need immediate funds. It’s like having a personal loan officer who already trusts you.

Interest sensitive lifestyles coverage, whether or not it’s CAWL or SPWL, offers a unique mixture of security and flexibility, permitting policyholders to adapt to lifestyles’s ever-converting panorama. By understanding the particular functions and advantages of each, you could tailor your existence coverage not just to meet your desires but additionally to paintings actively toward your financial desires.

Universal Life Insurance:

Universal life insurance is an interest sensitive life insurance that’s all about flexibility and control. Think of it as a versatile tool for your money management.

Here’s why it’s cool:

Flexible Premiums: Unlike other life insurance types, which require a fixed premium, Universal Life lets you adjust the amount you pay. Need extra money in some months? Pay more. Tight month? Pay less. As long as there’s enough in the account to cover the insurance costs, you’re good.

Adjustable Coverage: Life changes, and so can your coverage. Need more protection due to a new house or baby? Increase it. Kids all grown up, and the mortgage paid off? Decrease it. It’s life insurance that grows with you.

Interest-Sensitive Growth: The cash value of your universal life policy isn’t just sitting there. It grows based on current interest rates, potentially faster than a fixed rate in a whole life policy. This means more money building up over time that you can tap into if needed.

Tax Advantages: The cherry on top? The money you put in grows tax-deferred, and the death benefit your family receives is generally tax-free.

Universal life insurance is perfect for those who want a life insurance policy that adapts to their life’s twists and turns, offering a mix of protection, potential savings, growth, and flexibility.

Does Interest Sensitive Whole Life Insurance Affect Your Taxes?

Talking about taxes may not be as exciting as discussing the latest booze-worthy TV shows, but when it comes to under an interest sensitive whole life policy interest, discussing taxes is a bit more interesting—and definitely is not considered very useful.

100% income tax-free death benefit.

First up, let’s talk about the death benefit—this is the money your loved ones will receive when you’re no longer around. With interest sensitive whole life insurance, this payout is 100% income tax-free. That’s right, the IRS won’t touch a cent. It’s like leaving a final gift for your family that comes with a no-strings-attached tag from Uncle Sam. So, whether you leave behind $10,000 or $1 million, your beneficiaries get every penny. Think of it as your last “mic drop.”

Tax-deferred growth for your cash value account.

Now, onto the cash value—this is your policy’s growing financial pot that increases with interest over time. What’s cool here is that any growth in this cash value is tax-deferred. This means you don’t pay taxes on the growth as it happens. Instead, you only handle the tax bill if and when you withdraw more than what you’ve paid in premiums, which isn’t an everyday occurrence.

Key Benefits and Features of Interest Sensitive Whole Life Insurance

Faster Cash Value Growth: Your financial savings can grow faster with this type of coverage as it adjusts to the marketplace costs. When hobby charges go up, so does the increase in your money.

Tax-Free Death Benefit: The money your family receives once you pass away will not be taxed. This is a straightforward way to assist your circle of relatives financially without worrying about taxes.

Flexibility in Premium Payments and Death Benefits: This insurance allows you to adjust your monthly premium payment based on your current financial situation. You can also alter the amount your coverage can pay out when you die, as you wish.

Minimum Guaranteed Interest Rates: Your policy includes a minimum interest rate. This means that your savings will not fall below a positive amount, even if the marketplace drops. It’s like a safety net for your cash.

These features make interest touchy entire lifestyle coverage a bendy and steady choice, assisting you in manipulating your money higher and imparting it to your own family’s future.

Conclusion:

So, what’s the takeaway from an interest-sensitive whole life policy? It’s all about giving you more control and potentially more growth. Your premiums are flexible, your cash value grows with the market, and the death benefit is tax-free for your loved ones. If you’re looking for a life insurance plan under an interest sensitive whole life policy that adjusts to your life and the economy, this might be the smart move you need. Ready to let your life insurance work as hard as you do? An interest sensitive whole life policy could be your answer.

Refrences:

https://www.capitalforlife.com/glossary/interest-sensitive-whole-life

Meet Haider, our expert Life Insurance Content Writer and Editor. With a passion for clarity, he simplify the complex world of life insurance, delivering informative, polished content tailored to our clients’ needs.