Can You Get Life Insurance After a Stroke? Explore

Securing life insurance is a crucial step in planning for the future, and providing financial protection for your loved ones. However, if you’ve experienced a stroke, you might be wondering whether you can get life insurance after a stroke or not. The good news is that it is indeed possible to qualify for life insurance after a stroke, but the process can be more complex. Insurers consider various factors such as the type and severity of the stroke, your recovery, and your overall health post-stroke.

In this article, we’ll explore the details of getting life insurance after a stroke. We’ll explore the key factors insurers consider, provide tips to improve your chances of approval and discuss the types of policies that may be available to you. Understanding these aspects can help you navigate the process more effectively and secure the coverage you need for you and your loved ones.

Understanding Stroke and its Types

Stroke is a devastating condition when there is an obstruction or hindrance in the blood supply to the brain as a result of which brain cells perish. This may lead to tissue damage and impair brain function which changes into multiple symptoms, it totally depends on the brain area being affected.

There are two main types of stroke: ischemic stroke, on the other hand, is more prevalent while hemorrhagic stroke also happens occasionally.

1- Ischemic Stroke

This is the percent of all stroke types that is the most typical, which amounts to about 85%. This is precisely what can happen when a blood clot clips or significantly narrows a vessel that is thought to be the provider of the blood to the brain. The impairment of blood circulation means the oxygen and nutrients in the brain become deprived and cells die slowly.

Ischemic strokes can be further classified into two subtypes:

Thrombotic Stroke: This condition arises when a clot forms in one of the arteries that feed the brain blood.

Embolic Stroke: It can result from a clot that originated somewhere else in the body (most frequently in the heart) and travels towards the brain, ultimately obstructing a tiny blood vessel carrying oxygen and other vital elements needed for the brain’s proper functioning.

2- Hemorrhagic Stroke

The type of stroke which is caused by a blood vessel bursting or bleeding inside the brain is the most common kind of stroke. Blood escapes through the damaged veins and arteries, which puts pressure on the brain, impairing it. Hemorrhagic strokes can be further classified into two subtypes

Intracerebral Hemorrhage: This is due to the rupture of a blood vessel inside the brain and the accumulation of the blood flowing into the environment of the brain.

Subarachnoid Hemorrhage: This gets compressed when there is blood in the space between the brain and the enclosure.

Can You Get Life Insurance After a Stroke?

A question may arise in your mind after having a stroke: can you buy life insurance if you have had a stroke? Well! Yes, it is possible to obtain life insurance after a stroke, but the way how the process goes, and possible coverages are not the same and it is up to the factors to be varied.

Insurance companies try to figure out just how risky it is for them to be covering individuals who already had the stroke. They will look at the type of the stroke, its seriousness, your age, how well you’re doing in general, and how good you came back after it.

Here are some key points to consider if you’re looking to get life insurance after a stroke:

Time Since the Stroke:

The vast majority of insurance carriers will want to see how you have fared in the same time frame as your stroke, which is a period of ongoing monitoring for another several months to a few years.

Type and Severity of Stroke:

The insurers may differentiate between ischemic strokes (a blockage by an artery) and hemorrhagic (bleeding in the brain) strokes, not treating the same but being more flexible in ischemic stroke cases.

Recovery and Current Health:

At this point we will have a look into your general status of recovery and the specific lifestyle changes you might have made, discuss your medication plan and the follow-up care you have received.

How Much Does Life Isurance Cost?

Insurance Type:

This may vary depending on your particular situation -you may potentially be eligible for a regular life insurance or for a special type of insurance, like a guaranteed issue life insurance, that doesn’t require a medical exam but may come with costlier premiums and lower coverage amount.

You have to work with some independent insurance agent in the industry that will assist you in getting the needed details and looking for insurers that may be flexible for people who have experienced a stroke. Advising the doctor of the medical records in detail as well as a follow-up of the doctor’s guidelines can help as well in winning the life insurance coverage.

Best Life Insurance Plans for People Who Have Had Stroke

Having a stroke is not the end and there is no reason to feel suicidal. Life insurance options are available instead of giving up. Here are some options to consider:

1- Guaranteed Issue Life Insurance

In this insurance, regulations allow underwriting of coverage with no obligatory medical exam or health questions inquired. If you are eligible, you can benefit from the health insurance aging societies guarantee (the age usually starts at 50 and finishes around 80). But the premiums of the analyzed approaches are higher and the sum insured is lower than those of a typical life insurance.

2- Simplified Issue Life Insurance

This kind of policy needs you to respond to few health issues, compared to the guaranteed whole of life policy where the insurance company will require you to have a medical check-up examination. If your case is not a severe stroke and you don’t have any serious health problems, you may also be entitled to this insurance type.

3- Group Life Insurance

If you are employed, group life insurance available through employers in many cases may be a suitable option for you. Group policies are most of the time running the less strict or tighter underwriting required and can be more accessible by individuals who have gone through a stroke or cardiovascular event.

Shopping around between different insurance providers and comparing the price quotes will help one to get the best life insurance policy that suits their requirements. When one engages an independent insurance agent, he or she does not have to go solo because the agent is there to help with the process and finding the right coverage.

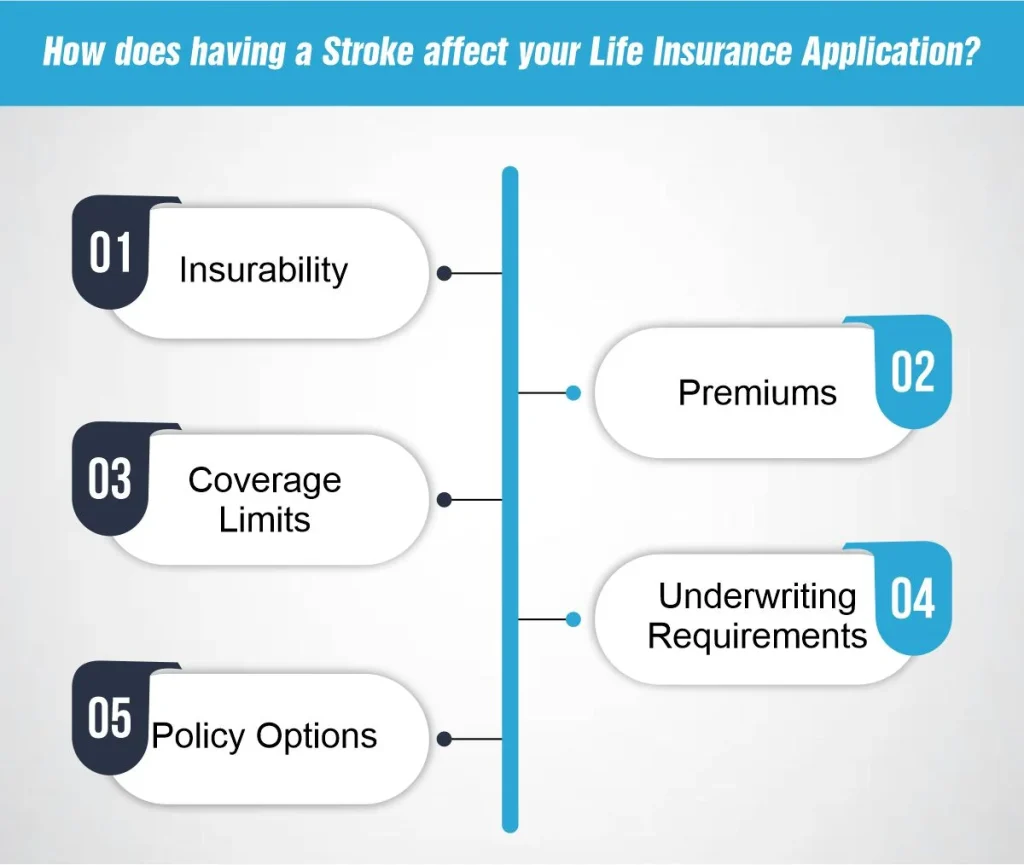

How does having a Stroke affect your Life Insurance Application?

How does having a Stroke affect your Life Insurance Application?

How does having a Stroke affect your Life Insurance Application?

How does having a Stroke affect your Life Insurance Application?Having a stroke can affect your life insurance application in several ways, including:

Insurability: The history of hemorrhagic stroke impair one’s ability to become eligible for the traditional life insurance. Insurers calculate the risk of covering individuals who had a stroke in relation to the stroke type and scale, but also based on your overall health.

Premiums: If your application is passed by the underwriters of the life insurance company after a stroke, it is very possible that you could have to pay a higher premium compared to a person with no previous stroke history. The quantum of premium hike you must fork out will be determined by variables such as attack type, severity, age, and total health.

Coverage Limits: Insurers may well restrict the maximum amount you can recover in relation to your stroke or exclude altogether from your coverage certain types of after stroke health problems. For instance, a patient may find that coverage does not include such things as future strokes or secondary illnesses related to a primary ailment.

Underwriting Requirements: Insurance companies might request you to submit your medical health forms and might also propose an additional medical examination or test which would help them to evaluate in detail your current health condition. In addition to the suggested treatment plan and medication regime, your relationship with them may also play a part.

Policy Options: If you are under specific conditions, the choice of policy type is a factor to consider because you may have fewer options than the policyholders at their disposal. You might proceed with guaranteed issue or simplified issue policies which may have higher premiums and lower coverage amounts to which you are likely to become eligible.

Final Thoughts

In the end, while a stroke can hinder your chances of being insured through a traditional form of life insurance, with the right information, you can still do so. Knowing the things that insurers are looking at helps you to fill the application forms properly. Things such as the type and the severity of the stroke, your recovery and your overall health are some of the key factors that insurers will check.

In addition the independent insurance agent, the revelation of complete medical history, and the compliance with physician’s recommendation can enhance the probability of you getting the coverage you desire. Taking the time to really analyze and evaluate your particular situation will allow you to choose a plan that is appropriate for you and provides protection for the later days.

FAQs

1- Can I get life insurance with a family history of strokes ?

You need to know that life insurance allows you to be insured even when you have a close relative with a history of stroke. While your rates may still fluctuate, just like other stroke survivors, multiple family members having the same medical condition may accelerate the increase of the rates.

2- If I’ve had a stroke, what questions will I be asked when I apply?

In a post-stroke life-insurance application, you may be asked about the kind of stroke, its severity, the exact day that it took place and the details of your recovery. Under their examination, besides current health status, they may also inquire about the side effects of the stroke, as well as your commitment to the medication and treatment.

3- What Happens To My Life Insurance Rates After A Stroke?

If the stroke results in the changes of the cardiovascular system (Medicine), your life insurance rates may increase since insurances deem you as a less eligible applicant. That concrete growth will be determined by factors that include level of stroke, its gravity as well as your overall health state.

References:

https://www.legalandgeneral.com/insurance/life-insurance/guides/life-insurance-and-strokes/

https://www.moneygeek.com/insurance/life/life-insurance-for-stroke-victims/

Expert Life Insurance Agent and health insurance agent

Dylan is your go-to guy for life and health insurance at InsureGuardian. He’s helped over 2,500 clients just like you figure out the best insurance plans for their needs. Before joining us, Dylan was sharing his expertise on TV with Global News and making a difference with various charities focused on health. He’s not just about selling insurance; he’s passionate about making sure you’re covered for whatever life throws your way.