Can your partner claim benefits: without your knowledge?

Have you ever wondered if your partner can claim benefits for you without your knowledge? This question touches on trust, privacy, and the rules that govern our rights. This topic is not only relevant but crucial for understanding how to protect and manage your benefits securely. What are the boundaries, and how can you ensure that your benefits are handled correctly and transparently? Let’s explore: Can your partner claim benefits for you without your knowledge to keep you informed and in control of your finances?

Can your partner claim benefits for you without your knowledge?

Generally, your partner cannot claim benefits on your behalf without your knowledge due to strict regulations designed to protect individuals’ rights and prevent fraud. Claiming benefits typically requires personal consent and identity verification directly from the individual whom the benefits will support. This procedure ensures that all claims are legitimately made and that benefits are appropriately allocated.

If a partner were to claim benefits without your knowledge, this could be regarded as fraudulent behavior, which is subject to serious legal repercussions. If you ever suspect that benefits might have been claimed in your name without your consent, it is crucial to promptly report this to the relevant benefit agency or social services. Taking this step helps safeguard your identity and ensures the proper handling of public or private assistance programs.

What do you need to apply for partner claim benefits?

Applying for partner claim benefits involves a specific process and requires gathering certain documents to ensure everything is handled smoothly and legally. Here’s a detailed breakdown of what you typically need to apply for partner claim benefits:

- Proof of Relationship: This is crucial as it establishes your connection to your partner. Documents such as a marriage certificate, a civil partnership certificate, or, in some cases, proof of cohabitation (like shared utility bills or lease agreements) may be required.

- Personal Identification: Both partners will likely need to provide valid identification. This could be a government-issued ID like a passport, driver’s license, or social security card.

- Financial Information: To assess eligibility, you should provide recent tax returns, pay stubs, employment details, and other financial statements. This helps the agency determine your household’s financial context.

- Application Forms: The required application forms must be filled out. These forms can usually be obtained from the agency managing the benefits. It’s important to fill these out accurately to avoid delays.

- Proof of Eligibility for Benefits: Depending on the type of benefit, you or your partner might need to provide evidence that you or your partner qualify. This could include medical records for health-related benefits, unemployment documents, or proof of a qualifying life event.

- Legal Documentation: Any legal directives, such as a power of attorney or a healthcare proxy that allow you to act on behalf of your partner should be included.

- Consent: Some jurisdictions may require explicit permission from both parties to process benefit claims, especially if one is acting on behalf of the other. Make sure to understand the consent requirements.

How Do Partner Insurance Benefits Work?

Partner insurance benefits are designed to extend insurance coverage from one individual (typically an employee or policyholder) to their partner. This can include various types of insurance, such as health, dental, life, and sometimes even auto or home insurance. Understanding how these benefits work can help you make informed decisions about your insurance needs and coverage. Here’s an easy-to-read overview of how partner insurance benefits typically function:

Eligibility

First, it’s important to determine who qualifies as a “partner” under the terms of an insurance policy. As previously mentioned, this could include:

- Legally married spouses

- Domestic partners (including same-sex partners)

- Civil union partners

- In some cases, long-term cohabitants who can demonstrate financial interdependence

Each insurance provider and policy might have specific criteria for who qualifies as a partner, so it’s essential to check these details.

Enrollment

To enroll a partner in an insurance plan, the primary policyholder often needs to provide:

- Proof of partnership (such as a marriage certificate or domestic partnership agreement)

- Identification documents for both parties

- Application forms during the insurance enrollment period or within a special enrollment period triggered by a qualifying life event (like a marriage or the establishment of a domestic partnership)

Coverage

Once enrolled, partners typically receive the same type of coverage as the primary policyholder. This can include:

- Health Insurance: Coverage for medical, dental, and vision care.

- Life Insurance: Beneficiary benefits in the case of the policyholder’s death.

- Disability Insurance: Coverage for lost income in case the partner becomes unable to work due to disability.

- Other Benefits: Depending on the policy, it might also include legal assistance, mental health services, or financial planning services.

Costs

Adding a partner to an insurance policy usually changes the premium cost. The total cost can depend on several factors, including the type of insurance, the coverage level selected, and the insurance provider. Sometimes, employers contribute a portion of the premium for the employee’s partner, but this varies widely.

Claims

Partners who are covered under these benefits can file claims in much the same way as the primary policyholder. For health insurance, this means visiting approved healthcare providers, paying any required copays at the time of the visit, and submitting claims through the insurance provider’s approved process.

How Much Does Life Isurance Cost?

Tax Implications

It’s important to note that depending on local laws, the premiums paid for a domestic partner’s coverage could be treated differently for tax purposes compared to those for a legally married spouse. In some cases, the premium amount could be considered taxable income.

Understanding these facts of partner insurance benefits can help you better navigate the specifics of your coverage, ensuring you and your partner are both adequately protected.

How do I know if I qualify for partner insurance benefits?

To determine if you qualify for partner insurance benefits, you’ll need to consider several factors specific to the insurance policy and the regulations of the insurance provider. Here’s a straightforward guide to help you understand your eligibility:

Type of Relationship:

Many insurance plans, especially health insurance, may require a legally recognized relationship, such as marriage or a registered domestic partnership. Some plans also cover long-term partners if proof of cohabitation (like joint bank accounts or utility bills in both names) can be provided.

Employer’s Policy:

If the insurance is offered through an employer, check their specific policy regarding partner benefits. Some employers offer inclusive benefits for domestic partners, while others might only provide coverage for legally married couples.

Residency Requirements:

Some insurance policies might have residency requirements that require the partners to live in the same household. You should provide proof of residency, like a lease agreement or home utility bills showing both names.

Duration of the Relationship:

Certain policies may stipulate a minimum duration for the relationship before a partner is eligible for benefits. This could be anywhere from six months to several years.

Financial Dependence:

Some insurance plans may require that the domestic partner be financially dependent on the employee to qualify for benefits.

State Laws:

Legal recognition of partnerships can vary significantly from one jurisdiction to another, especially concerning domestic partnerships, civil unions, and common-law marriages. Check local laws to see how they impact eligibility for partner benefits.

Plan Specifics:

Each insurance plan has its criteria for what qualifies someone for partner benefits. It’s important to read through the plan’s details or speak directly with a human resources representative or insurance agent.

Who is eligible for partner insurance benefits?

Eligibility for partner insurance benefits can vary based on the insurance provider, the type of insurance, and specific policy details. Here are some general guidelines on who might be eligible:

Legally Married Couples:

Almost universally, legally married partners are eligible to receive benefits from each other’s insurance policies, including health, life, and dental insurance.

Domestic Partners:

Many insurance plans now recognize domestic partnerships. To qualify, partners generally need to live together and share a domestic life, but they do not need to be married. Proof such as joint bank accounts, lease agreements, or utility bills might be required to demonstrate the partnership.

Civil Unions:

Similar to domestic partnerships, civil unions are legally recognized relationships that provide many of the same benefits as marriage. Eligibility for insurance benefits typically mirrors that of married couples.

Common-Law Spouses:

In places where common-law marriages are recognized, partners may be eligible for insurance benefits if they present themselves as married and meet specific criteria set by the state, such as living together for a specified period.

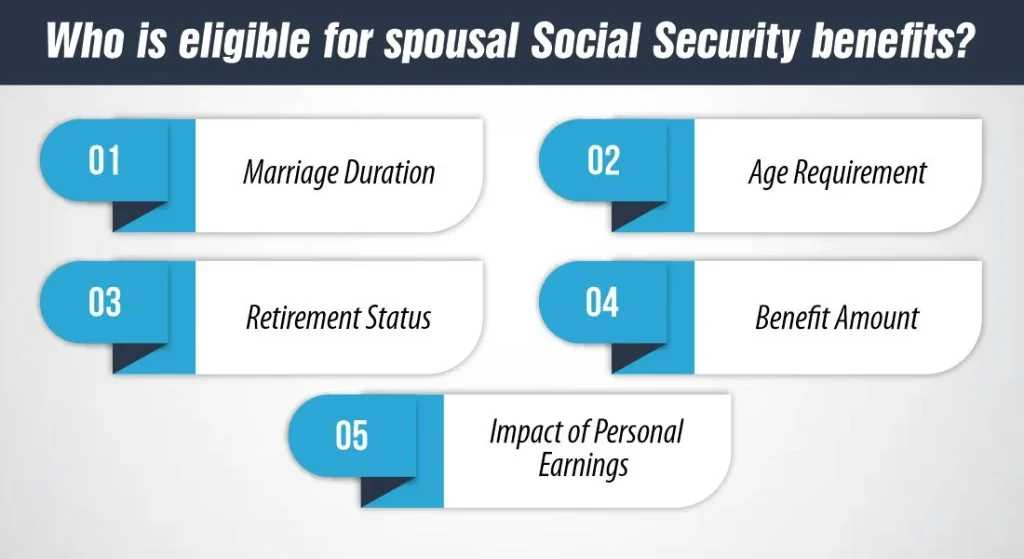

When should you claim partner benefits?

Deciding whether to assert partner benefits can be a big economic selection. Here are a few factors to take into account:

- Marital Status: You ought to be married to assert partner insurance advantages. If you are divorced, you may nevertheless be eligible if the marriage lasted at least 10 years, and you have not remarried.

- Age: You can declare partner insurance advantages as early as age 62, but your benefit amount could be reduced in comparison to ready until your full retirement age (generally between 66 and 67, depending on your beginning year).

- Your Earnings Record: If your own Social Security gain primarily based on your income records is better than the married gain, it could be greater high quality to claim your advantage.

- Your Spouse’s Earnings Record: If your spouse still needs to claim their personal Social Security benefits, you will be capable of declaring spousal advantages even by allowing your spouse’s benefits to keep growing till they attain their most at age 70.

- Health and Longevity: Consider your fitness and lifestyle expectancy. If you count on staying longer, delaying claiming spousal benefits might also bring about better general advantages over your lifetime.

- Financial Needs: If you want the profits sooner instead of later, claiming spousal benefits early can be important, even supposing it manner receiving a discounted advantage amount.

Consulting with an economic consultant or using online calculators allows you to decide the most appropriate time to assert spousal benefits based on your individual circumstances.

Strategies for Maximizing Spousal Benefits

Maximizing partner benefits can make a big difference in managing your financial and health-related needs. Here are some strategies tailored for specific situations, such as for late claimers, divorced spouses, and widowed spouses:

Strategy for Late Claimers:

If you’re a higher-earning spouse and you plan to delay claiming benefits until after full retirement age (FRA), your spouse may still be eligible for spousal benefits. However, it’s crucial to know that spousal benefits are reduced if claimed before the spouse’s FRA.

If your spouse is at their FRA and you’re delaying benefits, they can file for spousal benefits only if they still need to file for their benefits. By waiting until FRA, they can receive up to 50% of your full retirement benefit amount. However, if they claim before their FRA, their spousal benefits will be reduced.

To maximize the overall benefit, it’s essential to strategize based on both spouses’ ages, earnings records, and health considerations.

Strategy for Divorced Spouses:

Divorced spouses can claim spousal benefits based on their ex-spouse’s earnings record under specific conditions:

- The marriage must have lasted at least 10 years.

- The divorced spouse must be unmarried.

- The ex-spouse must be eligible for Social Security benefits (either retired or disabled).

- The divorced spouse must be at least 62 years old.

- The divorced spouse’s benefit must be less than the benefit they would receive based on their ex-spouse’s record.

If these conditions are met, the divorced spouse can claim up to 50% of their ex-spouse’s benefit amount. This can be advantageous, especially if the ex-spouse had a significantly higher earning history.

Strategy for Widowed Spouses:

Widowed spouses have several options to maximize benefits:

- They can claim survivor benefits as early as age 60 (or age 50 if disabled), but benefits will be reduced if claimed before their FRA.

- If the widowed spouse is already receiving retirement benefits on their record, they can choose to switch to survivor benefits if it results in a higher payment.

- Delaying survivor benefits until FRA or later can result in higher monthly payments.

- If the surviving spouse is caring for the deceased’s child who is under age 16 or disabled and receiving benefits, they can receive survivor benefits regardless of their age.

Understanding the nuances of survivor benefits and the impact of claiming decisions on lifetime benefits is crucial for widowed spouses to maximize their financial security.

Conclusion:

As we wrap up, Can your partner claim benefits for you without your knowledge? This would break the rules that are there to keep things fair and stop fraud. If you think someone has claimed benefits in your name without your permission, it’s important to report it right away. This helps keep your rights safe and ensures the benefits system works properly for everyone.

References:

https://www.hrblock.com/tax-center/irs/audits-and-tax-notices/someone-claimed-dependent/

https://wiserwomen.org/resources/social-security-resources/social-security-spousal-benefits/

https://www.bankrate.com/retirement/social-security-spousal-benefits/

Expert Life Insurance Agent and health insurance agent

Dylan is your go-to guy for life and health insurance at InsureGuardian. He’s helped over 2,500 clients just like you figure out the best insurance plans for their needs. Before joining us, Dylan was sharing his expertise on TV with Global News and making a difference with various charities focused on health. He’s not just about selling insurance; he’s passionate about making sure you’re covered for whatever life throws your way.