Life insurance types for construction workers: Best Types

There’s no doubt about it: Construction workers and laborers not only have some of the toughest jobs but also some of the most dangerous. When it comes to life insurance for construction workers and laborers, we find that many of them are severely underinsured for the type of work they perform on a daily basis.

When speaking with construction workers and laborer’s about life insurance coverage, a common concern is that many feels that they will pay a fortune for coverage or, worse, will not qualify for coverage at all due to their risky occupation.

The truth is the majority of construction and laborer jobs will be fine, qualifying for life insurance coverage without any penalties, extra fees, or high ratings. Applying and getting approved for life insurance as a construction worker or laborer is, in most cases, no different than any other civilian job.

Are you a construction worker or laborer with a high-risk occupation and are concerned about getting affordable life insurance coverage? And what are life insurance types for construction workers?

Looking to compare life insurance policies? We can help

Life insurance Types for construction workers:

- Roofer

- Brick layer

- Crane driver

- Civil Engineer

- Surveyor

Why is Life Insurance for Construction Workers Considered High Risk?

Life insurance for construction workers is regularly considered excessively dangerous due to the risky nature of the task. Construction websites are fraught with ability risks, including heavy equipment operation, work at heights, exposure to hazardous substances, and the danger of falling particles.

Insurance businesses assess risk based totally on the likelihood of having to pay a claim, and the excessive prevalence of place of business injuries in creation makes those regulations riskier to underwrite. Consequently, insurers may price higher charges for production employees to offset this improved risk. Moreover, some insurers may impose exclusions or barriers on guidelines for the creation of employees, similarly reflecting the dangerous conditions related to the enterprise.

Understanding those risks and the terms of their insurance regulations is vital for creating people who can ensure that they and their families are adequately financially supported.

Why Life Insurance for Construction Workers may be Even More Important than Other Occupations?

Life insurance is vital for construction employees, in particular, because of the excessive risks involved in their tasks.

Increased Risk of Workplace Accidents

Construction entails high-hazard activities, such as operating heavy equipment, climbing heights, and managing risky materials, which significantly increase the likelihood of injuries.

How Much Does Life Isurance Cost?

Financial Protection for Families

Life coverage offers vital economic safety for a production employee’s family in the event of a deadly accident, ensuring that they may not be harassed with monetary hardships after the loss of a top profit earner.

Coverage for Medical and Funeral Expenses

Life insurance guidelines can help cover medical bills and funeral fees, which may be large and difficult for households to manage suddenly.

Peace of Mind

Having lifestyle insurance offers construction people peace of mind, as they understand that their loved ones will be financially included if they are not around to offer help.

Encourages Safety Investments

Knowing the excessive fees related to lifestyle coverage charges may inspire both employees and employers to make extra investments in protection measures and education to lessen the likelihood of accidents and fatalities.

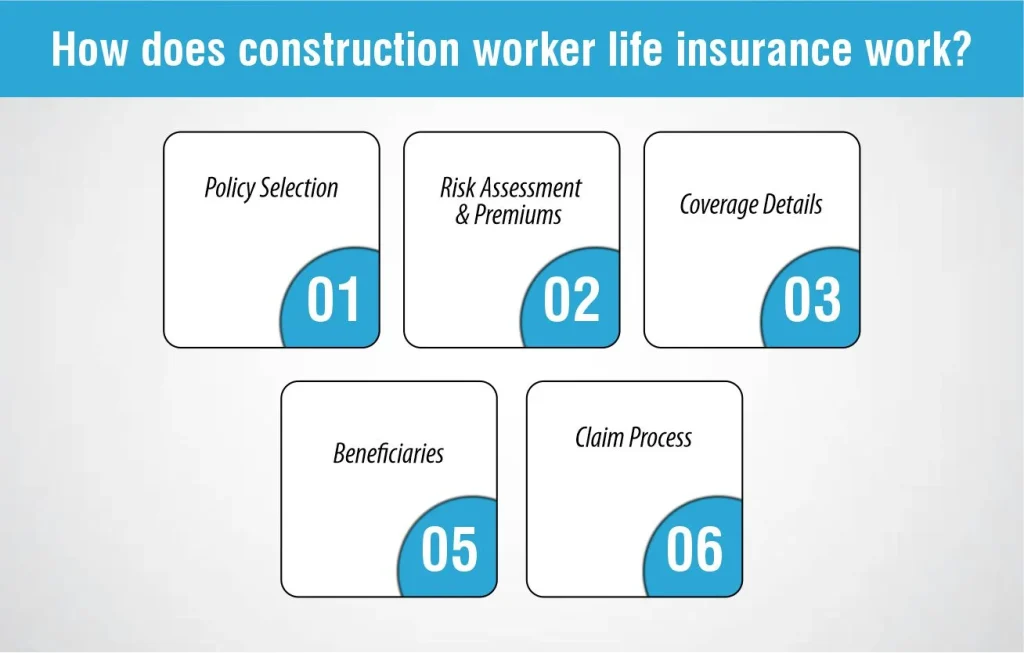

How does construction worker life insurance work?

How does construction worker life insurance work?

How does construction worker life insurance work?

How does construction worker life insurance work?Life coverage for construction workers’ capabilities in addition to standard existence coverage rules, but with considerations unique to the risks of the construction industry. Here’s the way it typically works:

Policy Selection:

Construction workers pick out existing insurance coverage that fits their needs, which is probably period life, complete existence, or every other sort of insurance. Term lifestyles insurance is famous as it may be aligned with the years an employee plans to be within the industry.

Risk Assessment and Premiums:

Insurers compare the risks related to the worker’s precise position in construction. High-risk roles may additionally cause better premiums—the everyday charge made to keep the coverage active—reflecting the extra chance of a declaration being made because of a place of business twist of fate.

Coverage Details:

The policy details how much money the coverage agency pays out (the death gain) if the worker passes away. This Amount is chosen when the coverage is bought and is meant to assist the employee’s beneficiaries financially.

Beneficiaries:

The employee names one or more beneficiaries—usually a circle of relatives members—who will get hold of the insurance payout within the occasion of the worker’s dying.

Claim Process:

In the event of a death, the beneficiaries file a declaration with the coverage agency. They must attach required files, like loss of life certificates. The insurer evaluates the declaration and, if accepted, issues the dying benefit to the beneficiaries.

Is critical illness cover available to construction workers?

Life insurance for construction workers is essential due to the high-risk nature of their job. These workers face a variety of risks every day, which makes securing financial protection through insurance critical. Here are some key points to consider about life insurance and additional coverage options available to construction workers:

Availability: Available to construction workers, providing a lump sum payment if diagnosed with a covered illness.

Common Illnesses Covered: Includes severe conditions like cancer, heart attacks, and strokes.

Considerations: Premiums may be higher due to job risks; policies could have exclusions specific to construction work.

Policy Review: Workers need to check for coverage specifics and exclusions that impact them.

Can construction workers get income protection?

Income protection is a crucial safety net for construction workers, providing financial stability when they are unable to work due to injury or illness. Given the physically demanding and hazardous nature of construction work, injuries are not uncommon, making this life insurance types for construction workers essential in the industry. Here’s how income protection for construction workers typically functions:

Coverage: The insurance provides a portion of the worker’s usual income when they can’t perform their job due to health issues. This payout helps cover daily living expenses and maintain financial stability.

Duration: Benefits from income protection can last until the worker is able to return to work, reaches retirement age, or for a set term specified in the policy.

Waiting Period: There’s generally a waiting period before benefits start, which can range from a few weeks to several months, depending on the policy details.

Premiums: The cost of premiums may be influenced by the level of risk associated with specific roles within the construction industry, as well as the worker’s health and age.

How much does construction workers’ life insurance cost?

This is a fairly common question, but unfortunately, there isn’t a single straight answer. How much you ultimately pay for life insurance will be based on:

- Your current age

- Your lifestyle, such as smoker status

- type of policy

- Length of cover (term)

- Amount of cover (sum assured)

Fortunately, it’s feasible to tailor your coverage to fit your wishes, making it clean to scale the fee of your month-to-month charges to shape your budget or increase the Amount of coverage to ensure your family is furnished.

Construction Insurance Types:

Here are different Life insurance types for construction workers of guidelines that defend against diverse risks associated with production projects and operations. Here’s a quick evaluation of not unusual production insurance kinds:

General Liability Insurance

This foundational coverage covers 1/3-birthday party claims of property damage or bodily harm caused by construction activities. It’s important to protect against injuries that could arise on a production website online.

Builders Risk Insurance

Builders’ danger coverage provides insurance for homes in production. It protects construction tasks from damage caused by events like fire, wind, robbery, or vandalism during the construction process.

Professional Liability Insurance

Also known as errors and omissions insurance, this protects construction experts against claims of negligence or failure to perform their expert responsibilities. It is vital for architects, engineers, and contractors who provide consulting and design services.

Workers’ Compensation

Workers’ reimbursement is mandatory in most states and covers scientific fees and a portion of misplaced wages for personnel who are injured or sick on the job. It’s critical insurance that also protects employers from court cases caused by injured employees.

Commercial Auto Insurance

This coverage covers cars owned by the construction company that might be used for painting purposes. It provides protection against liability claims and physical harm to cars involved in accidents.

Contractor’s Pollution Liability

Contractors’ pollution legal responsibility insurance is critical for construction projects involving environmental risk. It covers claims from pollutants caused by construction activities, including spills and contamination.

Can those who work in construction qualify for a traditional term or whole life insurance policy?

People who paint in construction can get traditional term insurance like term or whole existence guidelines, but there are some more matters to bear in mind. Because creation is a risky activity, insurance corporations may see those employees as a better threat. This way, they could have to pay more for their coverage. However, it is still possible for creation workers to get the coverage they need. They need to have a look at extraordinary coverage plans and recognize what everyone covers and does not cover. This way, they are able to pick out the excellent coverage that fits their task and affords accurate safety for their family.

What sort of data will the coverage businesses inquire from me or be curious about?

When making use of existence insurance, you will typically be asked to provide specified information about your employment and task obligations. If you work in the production industry, the insurance organization might also ask you questions about the unique obligations you carry out, the substances you deal with, and any hazards you may be exposed to during the process. They may additionally ask about your work environment, which includes any protection protocols that are in location.

Typical questions you’ll likely be asked may include:

- What kind of construction work do you do?

- How many years have you been working in this field?

- Do you hold any professional licenses?

- What is your exact job title?

- How many hours a week do you work?

In addition to this job-specific information, the insurance company may also ask you about your overall health and medical history. They will be interested in any pre-existing conditions, treatments, or medications you are currently taking. They may also ask about your lifestyle and habits, such as whether you smoke or drink alcohol and whether you engage in any high-risk activities, such as skydiving or rock climbing.

The insurance company will use this information and other factors to determine your risk profile and set the premiums for your policy. It’s important to be honest and accurate when providing this information, as any misrepresentation could result in a denial of coverage or a void policy.

Conclusion

In conclusion, life insurance for construction workers is vital due to the risky nature of their jobs. Various life insurance types for construction workers are available, including general liability, builders’ risk, professional liability, workers’ compensation, commercial auto, and contractor’s pollution liability. Each type addresses different risks faced on the job. Construction workers should carefully choose their insurance to ensure they and their families are well-protected financially. Understanding and selecting the right insurance can provide peace of mind amidst the daily risks of construction work.

FAQs

What can I do to help improve my chances of qualifying for the “best” life insurance policy for me?

To improve your chances of getting the best life insurance policy, focus on maintaining good health through regular check-ups and a healthy lifestyle, and accurately disclose your job details and medical history when applying.

What are the Levels of Risk for a Construction Worker?

Levels of risk for a construction worker vary from moderate to high depending on specific job duties, such as working at heights or with heavy machinery, which influence the terms and cost of insurance policies.

References

https://insurancebrokersusa.com/life-insurance-for-construction-workers/

https://www.annuityexpertadvice.com/insurance-a-construction-worker-needs/

https://iaminsured.co.uk/occupations/construction-industry-workers-life-insurance/

Expert Life Insurance Agent and health insurance agent

Dylan is your go-to guy for life and health insurance at InsureGuardian. He’s helped over 2,500 clients just like you figure out the best insurance plans for their needs. Before joining us, Dylan was sharing his expertise on TV with Global News and making a difference with various charities focused on health. He’s not just about selling insurance; he’s passionate about making sure you’re covered for whatever life throws your way.