Dave Ramsey Short Term Disability Insurance: Protect income

Are you thinking about short term disability insurance as a way to guard your profits in case of a sudden infection or injury? Dave Ramsey, a well-known monetary advisor, often discusses the significance of getting protected internet in the vicinity of such unexpected events. Short-term disability insurance can be a critical aspect of your economic planning, providing you with profit aid when you want it most.

This coverage is designed to cover a part of your income if you temporarily can’t work due to an incapacity, helping you maintain your financial balance without dipping into long-term savings or retirement funds. Before diving into Dave Ramsey Short Term Disability Insurance, it’s vital to understand what Dave Ramsey advises about the insurance stages, coverage terms, and the strategic function this type of insurance performs for your general financial fitness.

What Is Disability Insurance?

Disability coverage is a type of coverage designed to shield people financially in the event they’re not able to work due to a disability, whether it’s far as a result of a twist of fate or contamination. This coverage gives critical earnings aid by means of replacing a portion of the policyholder’s revenue at some stage in the length they are disabled, ensuring that their economic responsibilities, including mortgages, automobile bills, and everyday fees, can nonetheless be met.

Why You Need Disability Insurance?

- Income Security: The number one motive for having disability insurance is to steady a solid source of profits. At the same time, you are not able to earn a paycheck because of physical or intellectual fitness troubles. This is specifically crucial as your ability to paint and generate earnings is, in all likelihood, your maximum treasured economic aid.

- High Risk of Disability: Statistics recommend that a large portion of the workforce will experience a disabling condition before retirement. Disabilities are not always associated with risky sports or excessive fitness troubles; common conditions like back accidents, coronary heart disease, and other illnesses can also result in extended absences from work.

- Limited Government Support: While some may additionally consider that government programs like Social Security Disability Insurance (SSDI) may additionally suffice, those advantages may be restrained, challenging to qualify for, and won’t begin without delay. Moreover, SSDI may additionally provide a fraction of your preceding earnings.

- Employer Coverage May Be Insufficient: Although a few employers provide brief-time period or long-term disability insurance, those policies frequently only cover a part of your revenue and can have limitations. Personal disability insurance can complement those policies to offer greater comprehensive insurance.

- Covering Expenses and Debts: Daily living fees, clinical payments associated with the incapacity, and ongoing monetary obligations do not give up while your earnings do. Disability insurance helps cover these expenses, reducing financial stress for the duration of a tough time.

What Dave Ramsey Recommends for Disability Insurance?

Dave recommends getting coverage equal to 60-70% of your monthly income. To keep away from overpaying for insurance, he additionally shows that you choose the longest removal period your emergency fund and finances can take care of. The essential factor is that whether you’ve saved your first $ 1,000 or have your 3-to-6 months of charges stored for a rainy day, you may, without problems, pay the payments without risking your circle of relatives’ safety. He additionally recommends you opt for a gain period of up to age sixty-five or more if you may have the funds for it, but a five-year gain period will be the minimum suggestion.

Dave has stated that you need to get long-term disability insurance via your agency if they provide it. This option can commonly help you get better insurance for the least cash. But for individuals who don’t have this option, we can help you with price-effective disability insurance solutions with the proper amount of coverage to satisfy your needs.

How Much Disability Insurance Do I Need?

Start with the 60% to 70% of your monthly earnings that Dave Ramsey recommends. With this amount, you won’t need to live on rice and beans to cover your expenses. However, as you pay off your debts and boost your rainy day fund, you may reduce your coverage and revel in the monetary freedom of being partly self-insured.

How Long Should My Benefit Period Be?

A benefit length is the quantity of time you will receive payouts when they start. For long-time period disability insurance, Dave Ramsey suggests an advantage length of a minimum of 5 years and as much as age sixty-five if you may cover that financially. What’s going to happen after the next five years? The fact is that 85% of disabilities solve themselves within 5 years. By that point, your disability may be long past, or you may have taken up a new occupation you could perform with the disability.

How Long Should My Elimination Period Be?

An elimination duration is how long you have to wait when you’ve ended up disabled for your disability payments to begin. You do not need to overpay for insurance. If you may with ease sustain yourself for three, 6, or 12 months, it is commonly better to buy as much coverage as you want. Dave recommends that you now not pay more for coverage than you need to, so a ninety-day or one-hundred-eighty-day elimination period is recommended.

It’s well worth having a long-term period instead of Dave Ramsey Short Term Disability Insurance.

Opting for long-term disability insurance over short-term disability insurance is often considered a prudent economic choice for numerous vital reasons. While short-term disability insurance commonly covers you for a quick period—usually some months to a year—long-term disability insurance presents tons of extra full-size coverage, frequently lasting for several years or until retirement age.

Longer Coverage Duration:

The maximum considerable gain of long-term disability insurance is its duration. Many disabilities resulting from serious illnesses or accidents can last for years or even be permanent, some distance outlasting the insurance time period of quick-term rules.

How Much Does Life Isurance Cost?

Broader Financial Security:

Long-term disability insurance provides broader financial safety by replacing a portion of your earnings during prolonged periods of work incapacity. This can be critical for maintaining your lifestyle, meeting ongoing monetary responsibilities, and covering extra clinical costs related to long-term care or rehabilitation.

Peace of Mind:

Knowing you are protected for a longer duration provides colossal peace of thoughts, permitting you to be aware of healing without the introduced pressure of financial instability.

Cost-Effective in the Long Run:

Although long-term disability insurance can also have higher charges than brief-time period rules, it provides extra complete coverage over a more extended duration, making it a cost-effective preference ultimately, especially if you face a severe health problem.

Factors to Consider for Dave Ramsey Short Term Disability Insurance

Factors to Consider for Dave Ramsey Short Term Disability Insurance

Factors to Consider for Dave Ramsey Short Term Disability Insurance

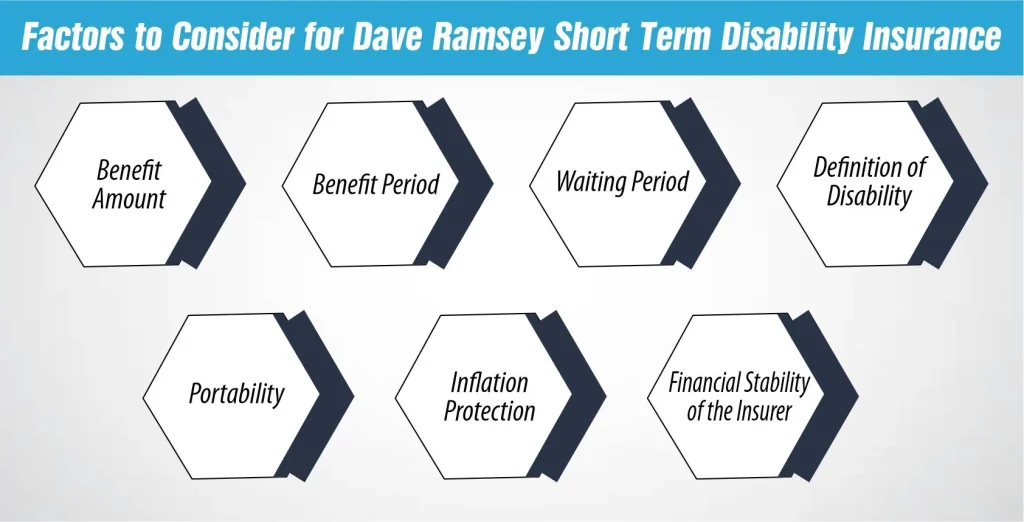

Factors to Consider for Dave Ramsey Short Term Disability InsuranceWhen choosing disability insurance, several key elements must be taken into consideration to ensure you pick the proper coverage for your desires. Here’s a quick review of critical issues:

- Benefit Amount: Determine how a great deal of your earnings will be replaced by means of the coverage. Most regulations provide between 50% and 70% of your pre-disability profits. Calculate how much you would want to satisfy your primary dwelling fees.

- Benefit Period: Consider how lengthy the policy will pay out blessings. Options range from some years to retirement age. Longer intervals typically mean higher charges; however, they provide more security.

- Waiting Period: Also called the removal duration, that is the time between when a disability happens and when advantages start. Shorter waiting intervals lead to better rates, so the stability of your economic reserves against potential needs.

- Definition of Disability: Policies vary in how they outline “disability.” Some cover you in case you need help to carry out your cutting-edge process, while others handiest pay if you can’t perform any job. The broader the insurance, the better the top class.

- Portability: If you convert jobs, can you take your coverage with you? This is essential in case your new corporation doesn’t offer disability coverage or if you plan to become self-hired.

- Inflation Protection: Consider whether the policy includes a cost-of-dwelling adjustment (COLA), which increases your advantage payout to keep up with inflation. This may be important for long-term benefits.

- Financial Stability of the Insurer: Check the insurer’s financial stability and claims payment history to ensure they can satisfy their obligations while you want them.

What you should consider before buying Dave Ramsey Short Term Disability Insurance:

Before purchasing Dave Ramsey Short Term Disability Insurance, there are numerous key elements to don’t forget to make sure that you have adequate insurance while managing costs correctly:

Build Your Savings:

Establishing a strong financial savings account can provide monetary cushioning in the event of disability. With good-sized savings, you could opt for a policy with an extended elimination period (the time earlier than benefits begin) or lower advantages that can reduce your top-class fees.

Coverage Duration:

It’s crucial to make sure that your policy’s advantage period—the duration of time you’ll get hold of bills—is enough for your desires. Most short-term disability guidelines cover some months to a year. Consider your hazard factors and economic scenario to determine if the insurance period is appropriate.

Policy Riders:

Adding riders to your coverage can provide extra blessings; however, it also increases the cost. Evaluate whether the fundamental insurance meets your wishes without extra riders. Dave Ramsey frequently suggests that a straightforward, no-frills policy is enough for maximum human beings, emphasizing the importance of a solid emergency fund over great coverage riders.

By thinking about those elements, you could make an informed decision that balances value with the security of getting insurance in case of Dave Ramsey Short Term Disability Insurance.

What Are the Types of Disability Insurance?

You will now see that there are two forms of disability insurance that are widely available: long-term and short-term. They essentially replace a portion of your monthly salary in a similar manner. But later, we’ll talk more about that.

There are certain distinctions between long-term and short-term disability insurance despite the fact that they serve the same purpose. This is how they compare:

| Comparison | Short-Term Insurance | Long-Term Insurance |

| How much does it cover? | Around 60–70% of your salary | 40–60% of your salary (but we recommend finding a policy that covers 60–70%) |

| How long does it last? | Usually 3-6 months —but that depends on the policy | Five years or longer if your disability continues |

| How much does it cost? | 1–3% of your yearly income (but tends to be more expensive than long-term coverage) | 1–3% percent of your yearly income |

| How soon would you get your first payout? | Around two weeks from when the doctor confirms you have a disability | Usually around 3-6 months |

| Why would you get it? | Only if your employer offers it at no cost to you | If you rely on your income and you don’t have savings to replace it long term |

Conclusion

Ultimately, by heeding guidance on Dave Ramsey Short Term Disability Insurance, you can greatly increase your financial readiness for unforeseen medical emergencies. Prioritizing the accumulation of a healthy savings account will allow you to more accurately determine your insurance requirements and choose a less comprehensive policy.

You can further reduce expenses and simplify your coverage by making sure the policy’s duration fits into your financial plan and by declining extra riders. In the end, including short-term disability insurance in your financial plan safeguards both your income and your peace of mind, freeing you to concentrate on your recovery rather than worrying about money.

FAQs

Is long-term disability insurance the same as long-term care insurance?

No, long-term disability insurance pays for expenses related to ongoing medical needs, such as in-home care or nursing facility care. It also replaces lost income in the event that an illness or injury prevents you from working.

Do you need disability insurance if you have a policy through work?

While having a disability policy through work is beneficial, it may not fully cover your income or last indefinitely. Evaluating the coverage limits and duration can help you decide if additional private disability insurance is necessary.

Do you need disability insurance if you have life insurance?

Yes, because life insurance provides financial support to your beneficiaries after your death, whereas disability insurance covers your loss of income due to disabilities that prevent you from working while you are alive.

References:

https://www.zanderins.com/dave-ramsey-recommends/disability-insurance

Expert Life Insurance Agent and health insurance agent

Dylan is your go-to guy for life and health insurance at InsureGuardian. He’s helped over 2,500 clients just like you figure out the best insurance plans for their needs. Before joining us, Dylan was sharing his expertise on TV with Global News and making a difference with various charities focused on health. He’s not just about selling insurance; he’s passionate about making sure you’re covered for whatever life throws your way.