State Regulated Life Insurance Programs: Legitimacy, Benefits and More

What Is a State-Regulated Life Insurance Program?

State-Regulated Life Insurance Programs, also known as State-Run Life Insurance or State-Backed Life Insurance, are insurance programs provided by state governments. These programs are designed to offer life insurance coverage to individuals who might not easily obtain coverage through traditional private insurance companies. They are typically aimed at helping those with health conditions that may be considered high-risk by private insurers or individuals with low income.

What sets State-Regulated Life Insurance Programs apart from private insurance is the state’s involvement. These programs are funded by the state and often carry certain eligibility criteria. They can be particularly appealing to individuals who find it challenging to secure life insurance through the private market.

How Does a State-Regulated Life Insurance Program Work?

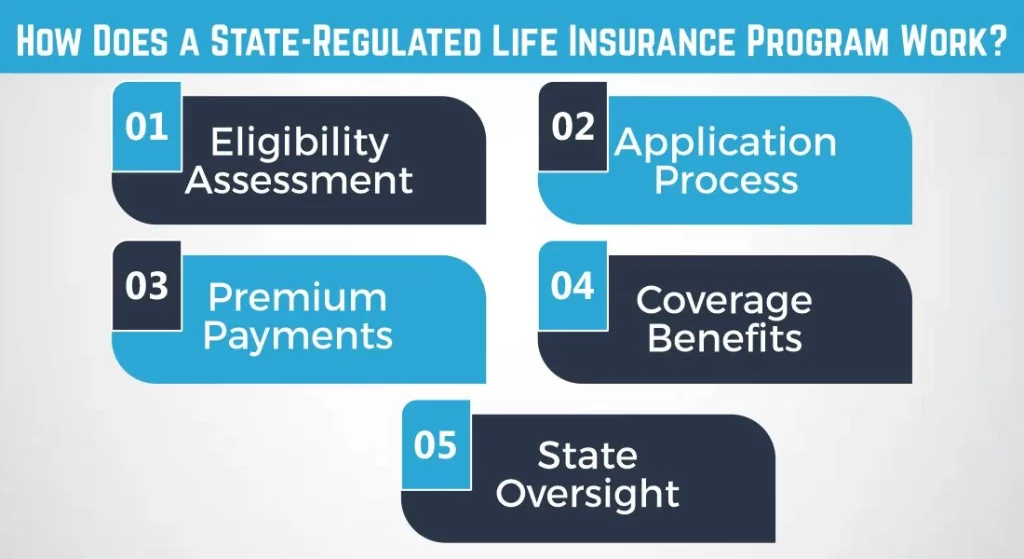

Understanding how State-Regulated Life Insurance Programs work is essential for making an informed decision. These programs typically involve the following key steps:

Eligibility Assessment: To qualify for a state-regulated program, individuals must meet specific eligibility criteria set by the state government. These criteria may include factors like income, health status, or age.

Application Process: Once eligible, you will need to apply for the program. The application process may require you to provide personal information and undergo underwriting.

Premium Payments: If approved, you will be required to pay regular premiums. The cost of these premiums is usually determined by your age, health condition, and the coverage amount you choose.

Coverage Benefits: State-regulated programs offer life insurance coverage, which means that if the policyholder passes away, their beneficiaries will receive a death benefit.

State Oversight: State governments regulate and oversee these programs to ensure that they meet their stated objectives and provide legitimate insurance coverage.

How Much Does Life Isurance Cost?

What Is the Cost of a State-Regulated Life Insurance Program?

The cost of a State-Regulated Life Insurance Program can vary widely depending on the specific program, the coverage amount, and the individual’s eligibility. In many cases, these programs offer affordable premiums, making life insurance more accessible to a broader range of people. However, it’s essential to understand that these programs may have limitations in coverage and benefits compared to private insurance options.

Here is a table to provide you a clear overview of the potential costs associated with a State-Regulated Life Insurance Program:

| Age Group | Monthly Premium | Coverage Amount |

| 18 – 30 | $20 – $50 | $50,000 – $100,000 |

| 31 – 45 | $40 – $80 | $50,000 – $150,000 |

| 46 – 60 | $60 – $120 | $50,000 – $200,000 |

| 61+ | $100 – $200 | $50,000 – $250,000 |

Please keep in mind that these numbers are estimates, and actual costs may vary depending on the specific State-Regulated Life Insurance Program, your health status, and other factors. It’s essential to contact your state’s insurance department or the program provider for precise and up-to-date pricing information tailored to your situation.

What Are the Benefits of State-Regulated Life Insurance?

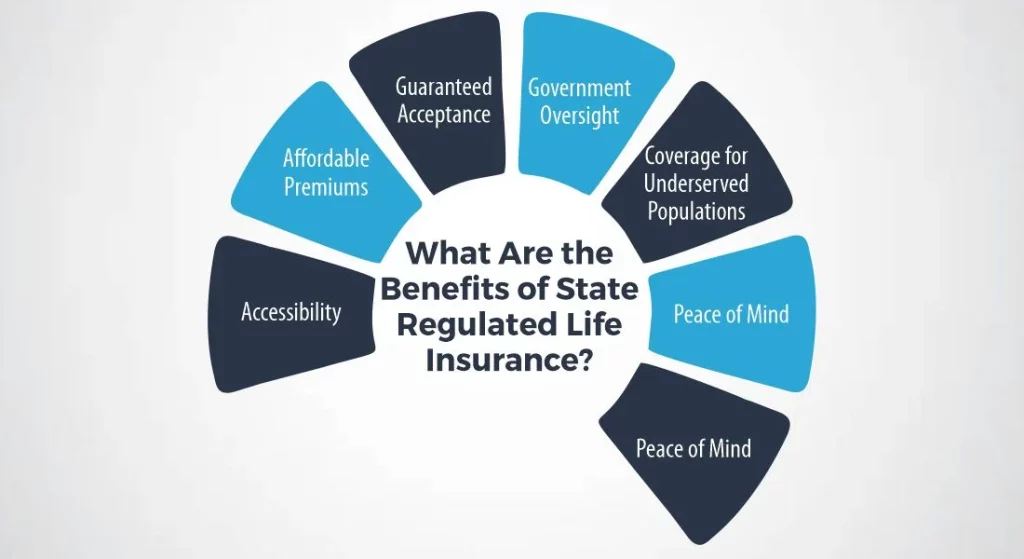

State-Regulated Life Insurance Programs offer several potential benefits, making them an appealing option for certain individuals. Here are some of the key benefits of these programs:

Accessibility

State-Regulated Life Insurance Programs are designed to provide life insurance coverage to individuals who may have difficulty obtaining it through traditional private insurers. This includes people with pre-existing health conditions or those with lower incomes who might not qualify for or afford coverage elsewhere.

Affordable Premiums

State-regulated programs often offer competitive premiums, making life insurance more affordable for individuals who might be on a tight budget. These lower premiums can be especially attractive to those who need coverage but have limited financial resources.

Guaranteed Acceptance

In some cases, these programs offer guaranteed acceptance, meaning you won’t be denied coverage based on your health condition. This is a significant advantage for individuals with serious medical issues who might face rejection from private insurers.

Government Oversight

State involvement in these programs adds an extra layer of oversight and regulation. This can provide a sense of security for policyholders, knowing that the program is subject to government scrutiny, which can help prevent fraud and ensure the program operates as intended.

Coverage for Underserved Populations

State-Regulated Life Insurance Programs are often targeted at underserved populations, addressing the insurance needs of those who might otherwise be left without coverage options.

Peace of Mind

By securing life insurance through these programs, policyholders gain the peace of mind that their loved ones will be financially protected in the event of their passing. This peace of mind is a significant benefit for policyholders and their families.

Flexibility

These programs may offer flexibility in terms of coverage options and premium payments, allowing policyholders to tailor their insurance to their specific needs and financial situation.

Expert Life Insurance Agent and health insurance agent

Dylan is your go-to guy for life and health insurance at InsureGuardian. He’s helped over 2,500 clients just like you figure out the best insurance plans for their needs. Before joining us, Dylan was sharing his expertise on TV with Global News and making a difference with various charities focused on health. He’s not just about selling insurance; he’s passionate about making sure you’re covered for whatever life throws your way.