Open Care Final Expense Plans review 2024

How Do Open Care Final Expense Plans Work?

Open Care’s final expense insurance plans provide a lump sum payment to the designated beneficiary upon the insured’s death. This payment can be used to cover end-of-life expenses, such as funeral and burial costs, as well as any other expenses the beneficiary may need to cover.

To enroll in an Open Care life insurance plan, the applicant typically needs to answer a few health-related questions, but no medical exam is required. Once approved, the policyholder pays a fixed monthly premium for the duration of the policy. This premium is typically guaranteed to be renewable for their lifetime.

If the policyholder passes away, the designated beneficiary will receive the agreed-upon lump sum payment. This payment can be used to cover any expenses related to their final arrangements or other financial obligations. However, the payment amount depends on the coverage amount and the policy’s specific terms.

Meanwhile, Open Care’s final expense insurance plans may have specific limitations and exclusions. These limitations and exclusions may include waiting for periods or restrictions on death causes. It is imperative to review the policy’s specific terms carefully and consult with a licensed insurance agent if you have questions or concerns.

Pros and Cons of Open Care Final Expense Plan

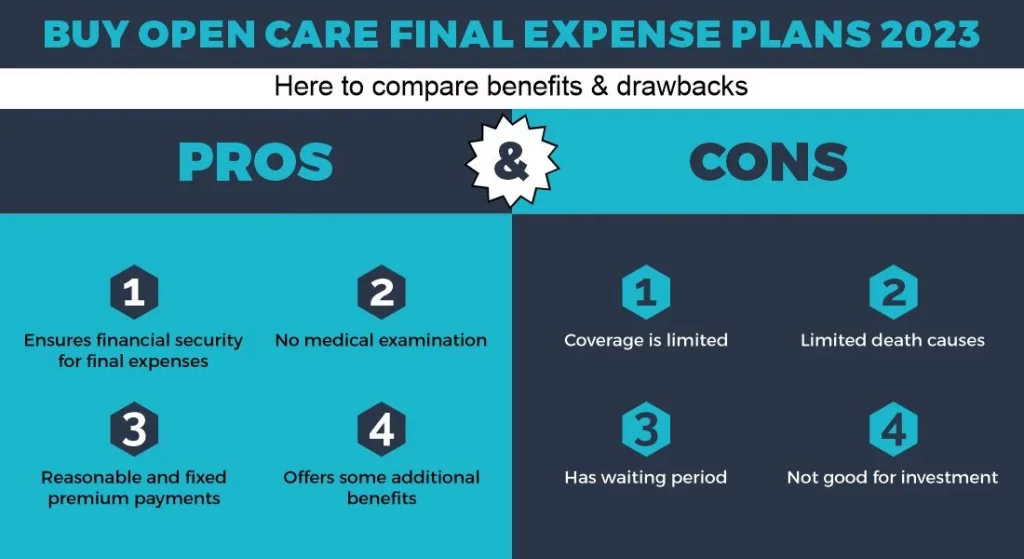

Here are some potential pros and cons of Open Care’s life insurance plan:

Pros:

Provides financial support for end-of-life expenses: The lump sum payment from the policy can help cover funeral and burial costs, relieving the financial burden on loved ones.

No medical exam required: Approval of the policy is based on answering health-related questions, which can make it more accessible to seniors with health issues.

Affordable and fixed premiums: The premiums are generally affordable and fixed for the policy’s duration, making it easier to budget for and plan around.

Additional benefits may be available: Open Care’s final expense insurance plans may offer additional benefits, such as accidental death coverage, which can provide additional financial support in difficult times.

Cons:

Limited coverage amount: The coverage amount for final expense insurance plans is typically lower than traditional life insurance plans, which may need more to cover all end-of-life expenses.

The waiting period may apply: Some final expense insurance plans may have a waiting period before the full benefit is available, limiting its usefulness in sudden death cases.

Restrictions on the cause of death: These plans may have exclusions or restrictions on the cause of death, which may limit the benefit paid out to the beneficiary.

Not an investment vehicle: Final expense insurance plans do not accrue cash value, which means they are not long-term investment vehicles.

Expert Life Insurance Agent and health insurance agent

Dylan is your go-to guy for life and health insurance at InsureGuardian. He’s helped over 2,500 clients just like you figure out the best insurance plans for their needs. Before joining us, Dylan was sharing his expertise on TV with Global News and making a difference with various charities focused on health. He’s not just about selling insurance; he’s passionate about making sure you’re covered for whatever life throws your way.